Support CleanTechnica’s work through a Substack subscription or on Stripe.

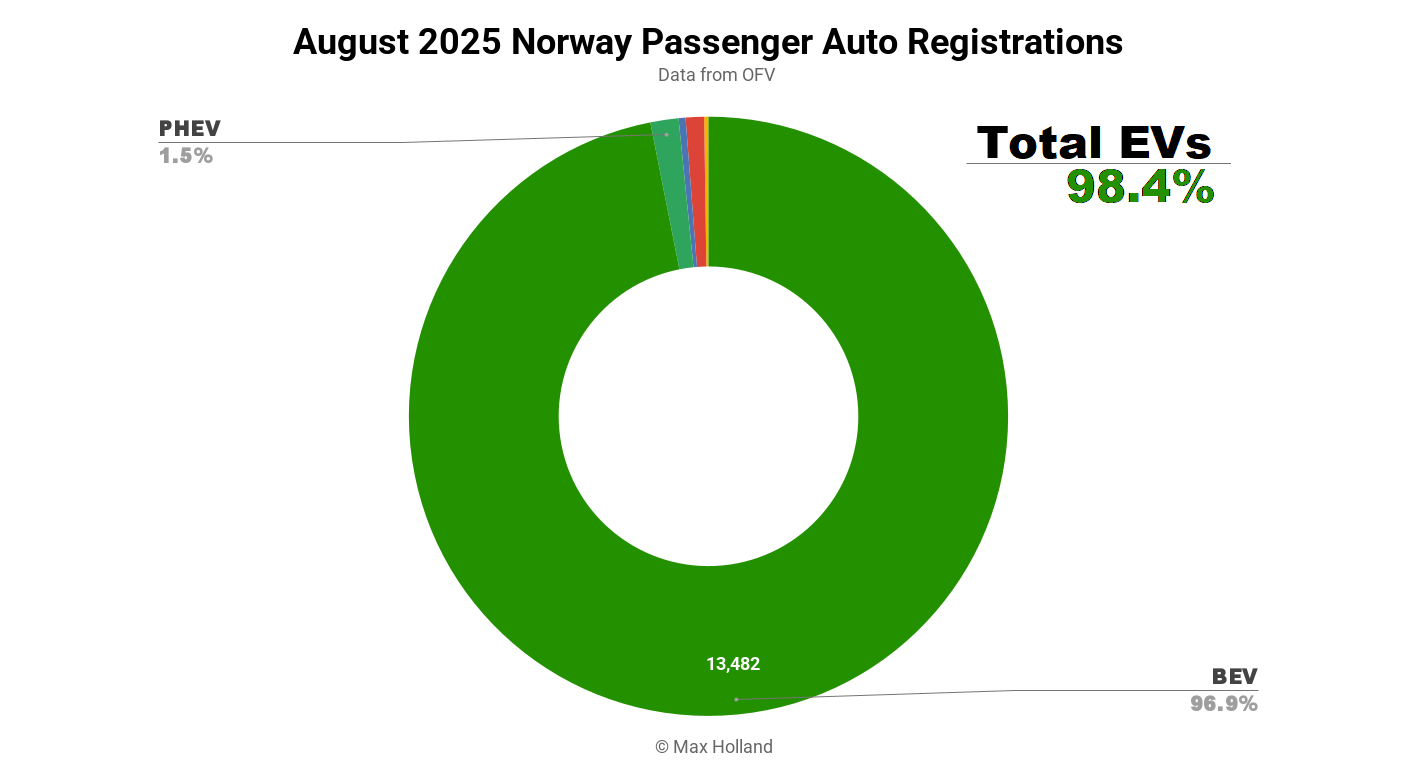

August saw plugin EVs at a record 98.4% share in Norway, up from 95.7% year on year. BEVs alone took 96.9% share. Overall auto volume was 13,915 units, up 25% YoY. The Tesla Model Y was the best-selling vehicle.

August’s sales totals saw combined EVs take a record 98.4% share in Norway, comprising 96.9% full electrics (BEVs) and 1.5% plugin hybrids (PHEVs). These compare with YoY figures of 95.7% combined, 94.3% BEV and 1.4% PHEV.

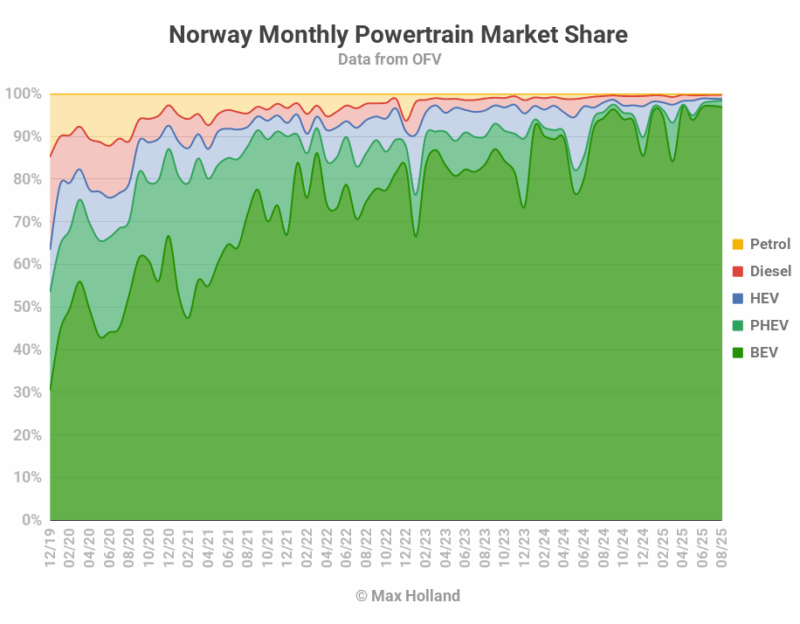

This is the third consecutive month of record share for EVs. The recent steady growth comes mostly as a consequence of HEVs and diesel-only vehicles being more strictly taxed for CO2 emissions, following policy changes enacted from April 1st. The continued growth is also the result of an ever broadening choice of competent and affordable BEV models available, displacing the ICE vehicles which were the only previous choices in those segments.

HEV powertrains (mainly sold by Toyota) have significantly eroded since April 1st, with their August share being just 0.4%, down from 2.2% YoY. Diesel-only are now down to 1.0% from 1.5% YoY, and petrol-only are now at 0.2% from 0.5% YoY.

Best-Selling Models

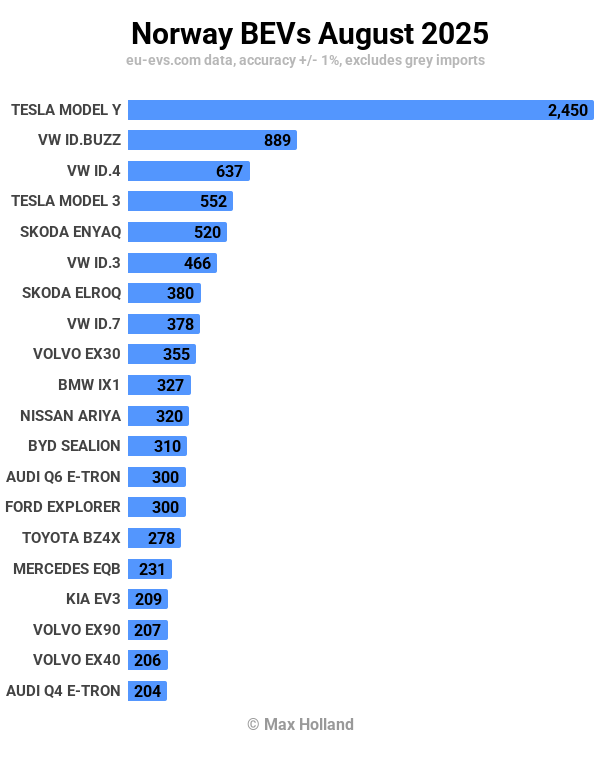

The Tesla Model Y was once again Norway’s best-selling vehicle, with 2,450 units, its sixth consecutive month in the lead.

The Volkswagen ID. Buzz took second place with 889 units, and its sibling the ID.4 took third with 637 units.

The Tesla Model 3 ranked 4th in August, due to a large push, though over the longer term it is trending down compared to a year ago. Back in mid 2024, thanks to the recent “Highland” refresh, the Model 3 was often in second place behind the Model Y. Even with August’s decent volume, its trailing 3-month rank is currently 6th, a long way from its past highs (more trailing-3 data below).

The Skoda Elroq continues its steady climb, following its first significant volume as recently as April. It saw a personal-best 380 units in August, ranking 7th (its highest yet). It’s a great value BEV, priced from 299,990 NOK (€25,500).

Other new-ish models which are doing fairly well include the MG S5 (March debut), which took a slight dip in August (to 29th), but may again place in the top 20 in the months ahead. Also the Zeekr 7X (April debut), which has delivered a consistent ~86 units per month recently, and ranks in the mid-30s region.

In the small-and-relatively-affordable segment, the Renault 5 and Hyundai Inster are still duelling for the lead. The R5 scored 115 sales in August, a new personal-best, and took 31st position. The Inster scored 98 sales, close to a personal-best, and ranked 35th. The Citroen e-C3 was not far behind with 81 units (39th).

The new Renault 4 (some 10% larger than the Renault 5) saw its first 5 units registered in August – these are likely showroom units, and we might expect customer volumes in October or November. The Nio Firefly still hasn’t had its retail launch, but the rumoured starting price will be 280,000 NOK (€23,800), about 12% above the Renault 5’s starting price. This pricing put it closer to the R5 than to the likes of the Fiat 500 and Mini BEVs, which are priced well above 300,000 NOK. I would thus expect the Firefly to be “a competitor” to the R5 (cross-shopped by prospective buyers).

The Opel Frontera, which launched in May, is selling around 60 units per month, and this is probably supply limited. Although a larger vehicle (4,385 mm), the Frontera’s entry price in Norway is 250,000 NOK (€21,300), about the same as the entry Renault 5 and Hyundai Inster, so will be considered by shoppers of those models.

It will be good to see more and more compelling and relatively-affordable models competing and together making up 5% (or more) of monthly BEV sales (and market share), and growing, with still more models coming (e.g. BYD Dolphin Surf).

Aside from the Renault 4 mentioned above, there were several other debutants in August. Perhaps the most important is the new Mercedes CLA, a D-segment sedan and Tesla Model 3 competitor, which has also just launched in Sweden (see that report for specs). The CLA registered just 8 initial units in Norway, but Mercedes will be hoping it gets to around 100 monthly units (or more), which would rank at least 30th spot.

The next most important debutants are two 4WD pickup truck models, something that many rural dwellers need, but with few options in Norway until now. The previous pickup truck choices were between an affordable (450,000 NOK) Maxus T90 that was limited to RWD only, or an expensive Ford F150 which started from 1,072,500 NOK (€91,200).

Maxus has now debuted the eTerron 9 pickup, selling 5 initial units. This is a large 5,500 mm pickup, dual-cab with AWD, a decent 3.5 ton towing capacity, and a 102.2 kWh battery. Pricing starts from 769,000 NOK (€65,400).

If that pricing still seems a bit rich, there’s an alternative in the form of the new KGM Musso Pickup (5 initial units in August). The Musso name has been around since 1993, initially as an SUV, and from 2002 as a Pickup. In its current BEV guise, it’s a dual-cab AWD pickup with a length of 5,160 mm, 1.8 ton towing capacity and an 80.6 kWh LFP battery. Pricing starts at 469,900 NOK (€39,900). If the lower towing capacity is adequate for a given user, the Musso appears to be the better value of these two new pickups, but we will see what their sales numbers reveal.

In other segments, Smart debuted their #5 mid-size SUV (with a length of 4,695 mm). Unfortunately Smart is barely selling in Norway at the moment (just 20 total units sold across all models this year), so don’t expect much impact from the #5. Additional issues are – that it starts at a higher price than the category giant, the Tesla Model Y, is unreasonably heavy for its size (over 2.3 tons), and is not very efficient.

There were a couple of debuts from Chery’s sub-brand Exlantix. I usually don’t jump straight in on small-volume Norwegian debuts from lesser-known Chinese brands, because these are often exercises in market research, rather than a volume launch aiming for ordinary consumers. If this brand later achieves strong volume (and a dealership network) in Norway, I will revisit these models.

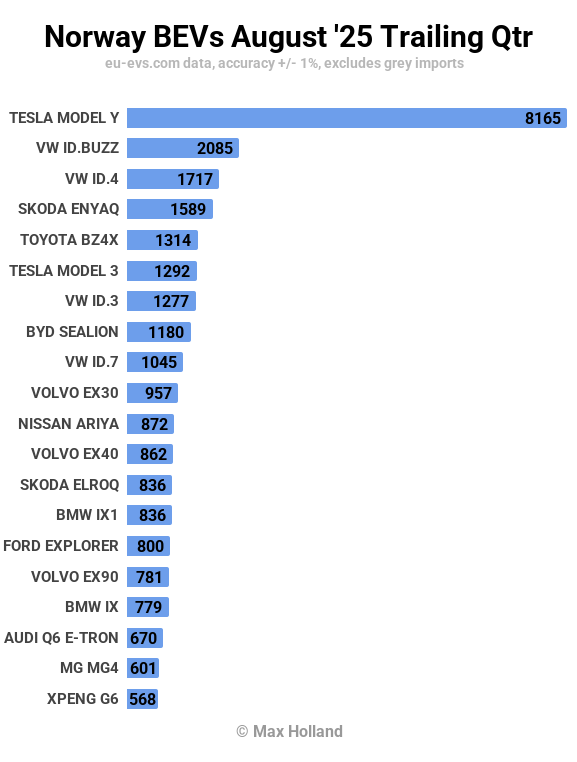

Let’s now turn to the longer-term sales rankings:

The dominance of the Tesla Model Y is clear, with more sales than the next 5 models combined (one of which is the Model 3). VW Group has an 8% volume lead over Tesla when summing all the respective models.

The notable climbs in ranking since the prior 3 month period come from the BYD Sealion (now at 8th, from 12th), the Skoda Elroq (13th from 26th), and the Volvo EX90 (16th from 23rd).

Further back, making steady progress outside the top 20, the MG S5 climbed from 41st to 26th, the Renault 5 from nowhere to 34th, and Zeekr 7X from nowhere to 37th. The Hyundai Inster is close behind, having now climbed to 38th. The MG S5 and the R5, and perhaps the Inster, potentially have the chance to break into the top 20 in the future.

Let’s also keep an eye on the progress of this month’s debutants, the Mercedes CLA, the Renault 4, as both of these could potentially join the top 20 next year.

For the latest update on Norway’s fleet transition, take a look at the June report.

Outlook

The April 1st tax changes have given a further bump to the EV transition in Norway. Helped by slightly lowered interest rates, and new BEV model offerings in affordable segments, as well as in underserved niches like rural pickups, plugless vehicles will soon comprise no more than 1% of the auto market. My expectation is that we may see the first month of 99% plugin share by the end of this year, or perhaps in Q3 next year.

Norway’s macroeconomic figures are often erratic due to the size of the public purse and the overweighting that fossil-fuel sales (and variable pricing) have on national bookkeeping. YoY GDP figures took one of their occasional wild swings in Q2 2025, with negative 2.1%, albeit from an anomalously high growth figure in Q2 2024. Inflation crept up to 3.3%, and interest rates remained flat at 4.25%. Manufacturing PMI dropped to 49.6 points in August, from 51.1 in July.

A bright spot for the fleet transition is the growth in BEV sales compared to a year ago – year to date car sales (now almost all BEV) are up over 25%. This indicates a faster-than-normal retirement of older ICE cars, and an acceleration of purchases of the new technology. What are your thoughts on Norway’s auto market? Please jump in to the comments below to share your perspectives.

Sign up for CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy