Support CleanTechnica’s work through a Substack subscription or on Stripe.

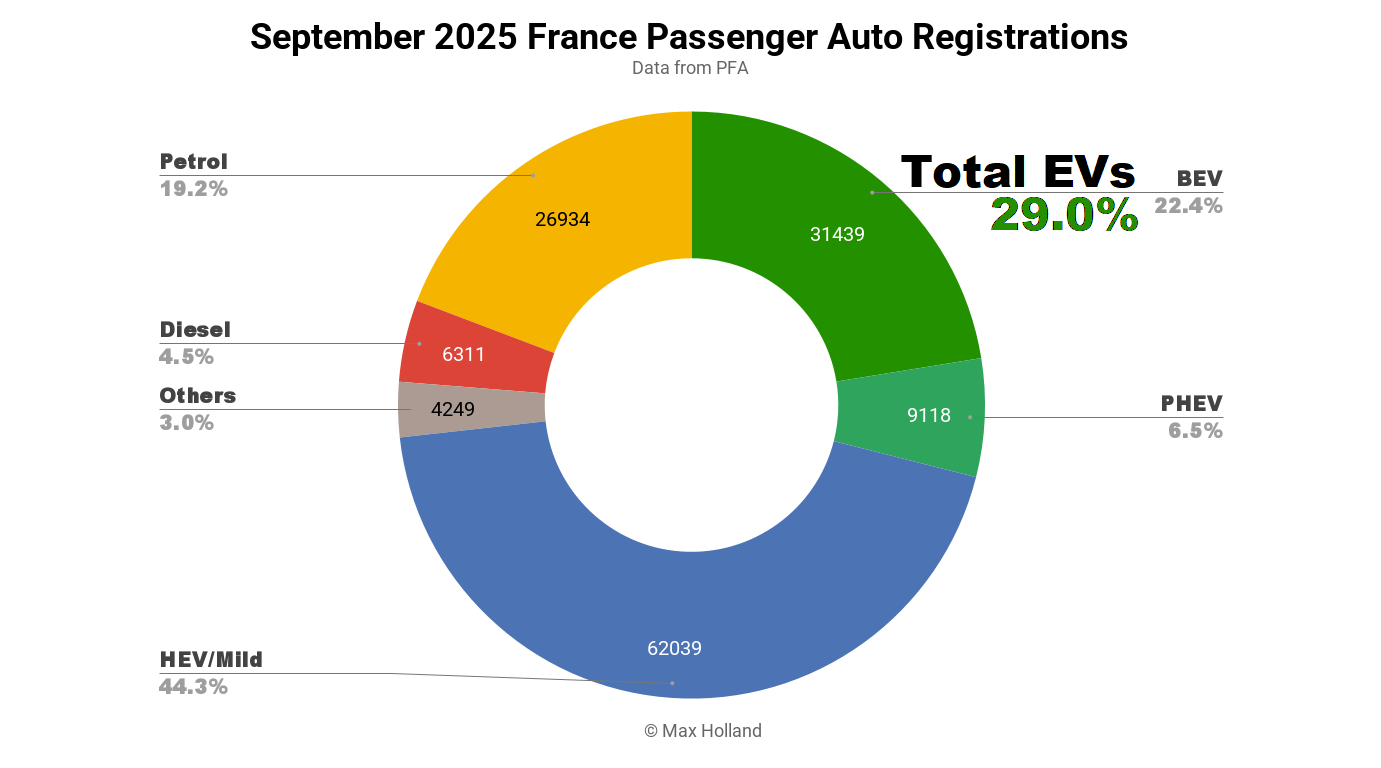

September’s auto sales saw plugin EVs take 29.0% share in France, up from 27.6% year-on-year. BEVs grew volume and share, and PHEVs dipped. Overall auto volume was 140,090 units, flat YoY. The Tesla Model Y was the best-selling BEV, with its largest monthly volume in two years.

September’s auto sales totals saw combined plugin EVs take 29.0% share in France, with 22.4% full battery-electrics (BEVs) and 6.5% plugin hybrids (PHEVs). These compare with YoY figures of 27.6% combined, 20.4% BEV and 7.2% PHEV.

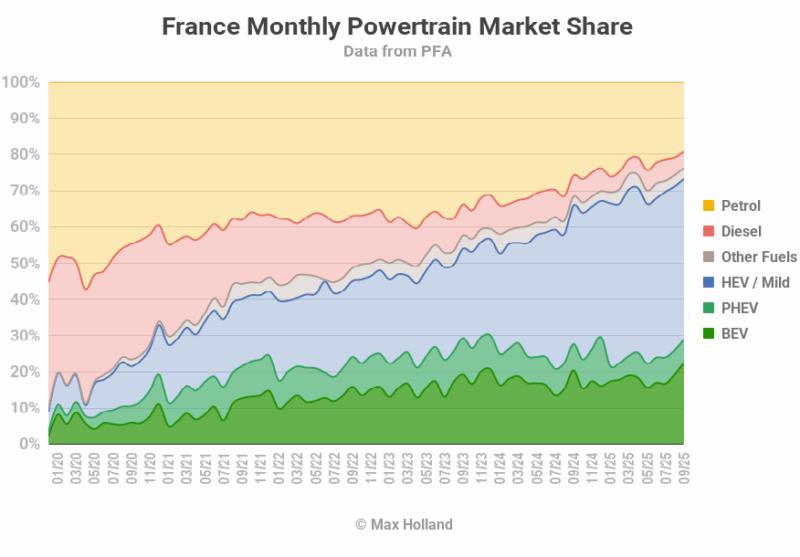

Looking more broadly at the cumulative year-to-date performance, combined plugin share now stands at 24.3%, with 18.2% BEV, and 6.1% PHEV. The equivalent market shares at this point in 2024 were 25.0%, with 17.1% BEV and 7.8% PHEV.

We can see that whilst BEVs have grown marginally (adding 1.1% market share), PHEV share has diminished more (losing 1.7%), leading to a combined deficit of 0.7% – not a great result. However, although BEVs were down YoY across H1, they’ve had a modest turn around in Q3, selling 67,978 units, up by 16.3% compared to Q3 2024.

What factors are now in play, and how will they shape the remainder of the year? The 2025 “Social Leasing” programme is now in effect (from 30th September), with up to 50,000 vehicle leasing contracts able to get leasing support from the Government. Prior to this date, in the period since it was confirmed in late June (i.e. July, August and September), some number of BEV purchases will have been held-back. This circumstance makes the Q3 growth a decent result.

Recall, however, that the leasing programme is deliberately narrow in scope, and is thus unlikely to have a “massive” impact on the BEV market, though likely a noticeable one. It is aimed exclusively at low-income buyers (earning under €16,300 per year), and the vehicle must be used for commuting or professional activity, and cover at least 8,000 km per year.

At the time of writing, it seems likely that most of the scheme’s 50,000 unit cap will have been exhausted in a rush of signings over the past week or so. Note that the actual deliveries of these leased vehicles will come more gradually over the next few months.

Given the additional boost from the leasing programme, BEVs should end full-year 2025 close to 20% share, up from near 17% in both 2024 and 2023, and from 13% in 2022. This is not dramatic progress, but at least puts France back on a growth path. For context, the German market looks set to end the year with BEV share around 19%, and the UK market will see BEVs end this year at close to 25%.

With the remaining ICE-only sales also being quickly eroded via substitution by mild-hybrids and HEVs, September saw ICE-only share hit a new record low of 23.7%. Petrol-only fell under 20% for the first time, at 19.2% share. December should see combined ICE-only falling under 20% of the market for the first time.

![EVs Take 29.0% Share In France]() Best-Selling BEV Models

Best-Selling BEV Models

Best-Selling BEV Models

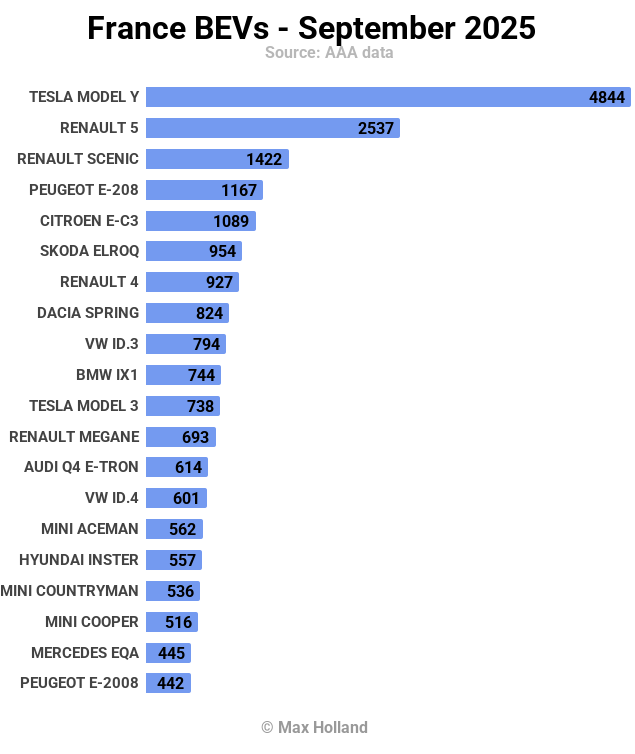

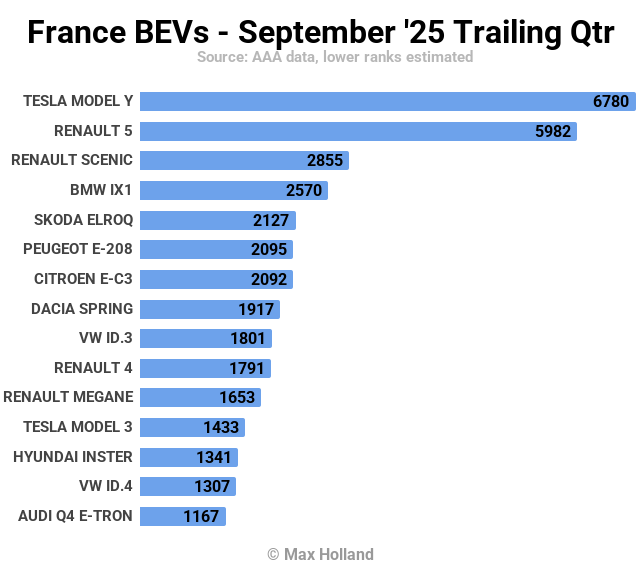

Best-Selling BEV ModelsAfter having been down in YoY volume by around a third in recent months, the Tesla Model Y finally made a strong comeback in September, with a huge 4,844 units. This was its highest volume in two years, and equated to roughly the sales of the next three BEV models combined.

The ever-popular Renault 5 came in second, with a decent 2,537 units, and its sibling the Renault Scenic came third with 1,422 units.

The overall line up of faces remains familiar, with mostly modest variations in relative ranking compared to recent months.

The overall line up of faces remains familiar, with mostly modest variations in relative ranking compared to recent months.

The Skoda Elroq is still climbing in volume, seeing a personal-best 954 units in September, retaining 6th spot. Now just behind, in 7th, the new Renault 4 also hit a strong PB, with 927 units, greatly up from its previous high of 539 units (June). On its current trajectory, the Renault 4 still has room for more growth, and looks set to potentially overtake the Elroq in the coming months.

Further back, the Hyundai Inster also kept growing, hitting a new high of 557 units (up from 448 in August), and taking 16th spot. The BYD Dolphin Surf is still staying in the wings for now, not being visible in the top 20 since its initial splash back in May.

European production of the Dolphin Surf (in Hungary) will begin in early 2026, likely re-opening BYD’s eligibility for French incentives and avoiding some EU tariffs. It may be that BYD is waiting for this European production before making a volume push in France.

BEV models with MSRPs starting under €30,000 (and under €25,000 in some cases) are quickly approaching half of all BEV sales, just as small-and-simple cars have traditionally dominated the overall French auto market.

As usual, model sales data is limited for the French market (to roughly the top 20 only), preventing us from detecting low-volume debuts of newer BEV models. Keep an eye out for the reports from adjacent markets, to get a sense of what new models are arriving.

Let’s now turn to the 3-month rankings:

We can see that the Model Y has retaken the lead over the Renault 5, which led last month’s trailing-3 chart. Thanks to the strong September, the Model Y increased its volume by 62% over the prior period (Q2), when the Renault 5 dominated.

The biggest overall climbers are the Renault 4, and the Hyundai Inster. The Renault 4 had only just debuted in the Q2 period, and ranked 22nd, with under a thousand units sold. In Q3 it shifted 1,791 units, and climbed to 10th. It still has room to grow.

Likewise, the Hyundai Inster had barely debuted back in Q2, with only low hundreds of units sold, well outside the top 20. In Q3 it gained 1,341 sales, and climbed to 13th spot.

Both these two models, as well as many other small-and-affordable BEVs, will get a further boost from the Social Leasing Programme in the coming months.

Outlook

Following on from the first month of positive auto market growth in August, September was the second time this year when the overall auto market was not negative (though 0.8% YoY growth is only barely positive).

The broader macroeconomy reflects this lack of energy, with latest Q2 2025 data showing 0.8% YoY GDP growth, following the weakness in Q1 2025 and Q4 2024. Headline inflation increased to 1.2% in September, from 0.9% in August. ECB interest rates are still 2.15% (steady since early June). Manufacturing PMI dropped steeply, to 48.0 points in September, from a short-lived blip of 50.2 points in August.

France’s political leadership remains unpopular, with Macron at an approval rating of just 17% according to recent polling, but refusing to call fresh elections, and e.g. failing to speak up with any conviction about the genocide in Gaza, according to his political opposition, leading to widespread street protests. None of this is helping France’s confidence about the future, prospects of economic sentiment improving, nor the country’s preparedness to embrace changes like the adoption of EVs.

What are your thoughts about France’s auto market and the transition to EVs? Which models have you got your eye on as they climb the ranks? Please share your thoughts and perspectives in the comments below.

Sign up for CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy