As retailers rush to stock up ahead of expected tariff increases, import volume at the nation’s major container ports is forecast to hit a new all-time record this month, according to the Global Port Tracker report released today by the National Retail Federation (NRF) and Hackett Associates.

That surge will likely come because temporary 10% Section 122 global tariffs that took effect in February are set to expire July 24, but a new round of tariffs regarding forced labor are expected to be imposed by the Trump administration as early as August.

In response, the May through July numbers are expected to be the highest of the year. The peak shipping season, which historically centered around October, has moved up in recent years amid reasons ranging from port labor disputes to expected tariff increases, NRF said.

“This year’s early peak season is expected to continue through July as retailers and other importers prepare for potentially higher tariffs beginning in August and other trade uncertainties,” NRF Vice President for Supply Chain and Customs Policy Jonathan Gold said, noting continued supply chain impacts from the conflict in Iran. “The busy back-to-school selling season has already started, and the winter holidays won’t be far behind, so retailers have been working to get products into the U.S. and ready to go before new tariffs can potentially drive prices higher. Despite ongoing economic headwinds, consumers are continuing to spend, but affordability is a key factor affecting their spending habits.”

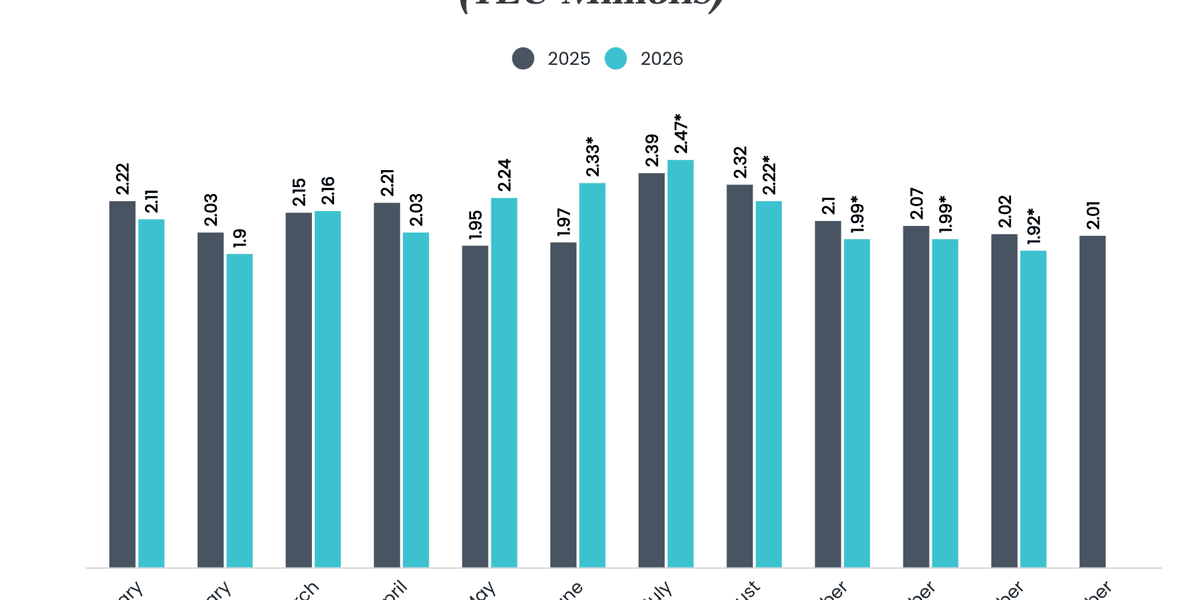

By the numbers, U.S. ports covered by Global Port Tracker handled 2.24 million twenty-foot equivalent Units (TEU) in May, the latest month for which final numbers are available. That was up 14.9% from a year earlier, when imports were down sharply because of last year’s “Liberation Day” tariffs, and up 10.1% from April.

Ports have not yet reported June numbers, but Global Port Tracker projected the month at 2.33 million TEU, up 18.7% year over year. That would bring the first half of 2026 to 12.77 million TEU, up 2% from the same period in 2025.

July is forecast at 2.47 million TEU, which would be up 3.3% from last year and would top the previous monthly record of 2.4 million TEU set in May 2022 as the economy bounced back from the pandemic. Imports are expected to drop to 2.22 million TEU in August, down 4.5% year over year. September is forecast at 1.99 million TEU, down 5.7% year over year; October also at 1.99 million TEU, down 3.8%, and November at 1.92 million TEU, down 5.2%.