The effects of oil price shocks are rippling through shipping markets, with Q2 data showing fuel rates actualized at higher-than-projected levels and Q3 estimates predicting rates will stick at elevated levels or even higher, due to renewed conflict in the Middle East, according to a report from AFS Logistics and TD Cowen.

Those trends come from data in the third quarter (Q3) 2026 release of the TD Cowen/AFS Freight Index, a snapshot with predictive pricing for truckload, less-than-truckload (LTL) and parcel transportation markets.

“With this edition of the freight index, the fuel numbers tell the story. In Q2, diesel prices rose about 51% compared to January and February levels, while jet fuel prices were up 90% compared to Q2 of last year,” says Andy Dyer, CEO, AFS Logistics. “Beyond the direct impact of higher freight bills paid by shippers, these price movements also have second-order effects that squeeze rates higher. Smaller truckload carriers working on tight margins may park trucks and wait for fuel prices to revert to more palatable levels before returning to operation, further restraining capacity amid a supply-side market correction.”

The report broke out those impacts into three sectors:

** Truckload rates jumped to their highest levels in 15 quarters despite modest cargo demand, due to a mixture of spiking fuel costs and a constrained supply of truck drivers. Industry freight capacity has tightened following the Trump Administration’s heightened regulatory enforcement actions that have reduced the driver pool by more than 48,000 people over the past year, the report said.

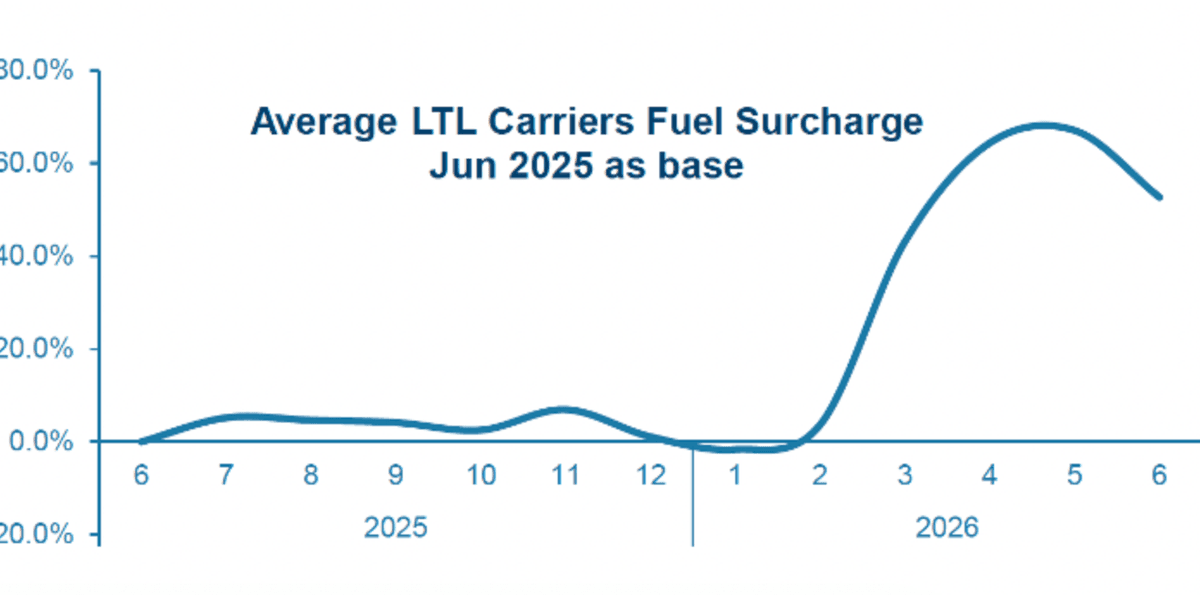

** In less than truckload (LTL), data showed falling weight-per-shipment reflecting continued softness in industrial and manufacturing demand. But rates surged anyway, due to 51% higher diesel prices compared to the early 2026 average, which were primarily driven by the prolonged conflicts in the Middle East. That pushed the average LTL fuel surcharge in Q2 to rise over 60% above the June 2025 level.

** The parcel segment is due for a new era of competition, because of the emergence of viable alternative carriers for regional and last-mile delivery, such as OnTrac, GLS, Spee-Dee, Veho, and UniUni, which together more than doubled their volumes from 2024 to 2025. At the same time, the sector will be impacted by Amazon Supply Chain Services opening its network to external shippers, which could have “meaningful” long-term implications for the pricing power of FedEx and UPS.