Support CleanTechnica’s work through a Substack subscription or on Stripe.

After the usual December EV record sales peak in China, which coincided with an end-of-incentive sales rush (NEVs are no longer exempt from purchase tax this year), the year started with an expected sales slump, down by 20%, which sounds like a lot, but considering that the overall market was also down 14% YoY, to 1.5 million units, it doesn’t sound all that bad.

BEVs were down by 17% YoY in January, to 348,000 units, while the PHEV drop was even harsher (-24%), at 248,000 units. Of these, 76,000 were EREVs, which is one of the few bright spots of January. The extended-range electric vehicle market was actually up 1% YoY, thanks to the popularity of this kind of powertrain in large SUVs, which was the category less affected by the end of incentives.

This allowed plugin vehicle (PEV) share to start the year at a high 39% (23% BEV), more or less aligned with January ’25, which is good news considering the loss of incentives. Although this score is well below the final 2025 result of 54% PEV share (33% BEV), expect that mark to be achieved sometime in the summer, and the year to end around 60% share. A couple of months in the last quarter of the year should even end above 65% share.

Imagine that — the largest automotive market in the world with a 66% plugin share. These kinds of market shares would be considered a pipe dream when I started reporting EV sales back in 2012….

{kind=link}

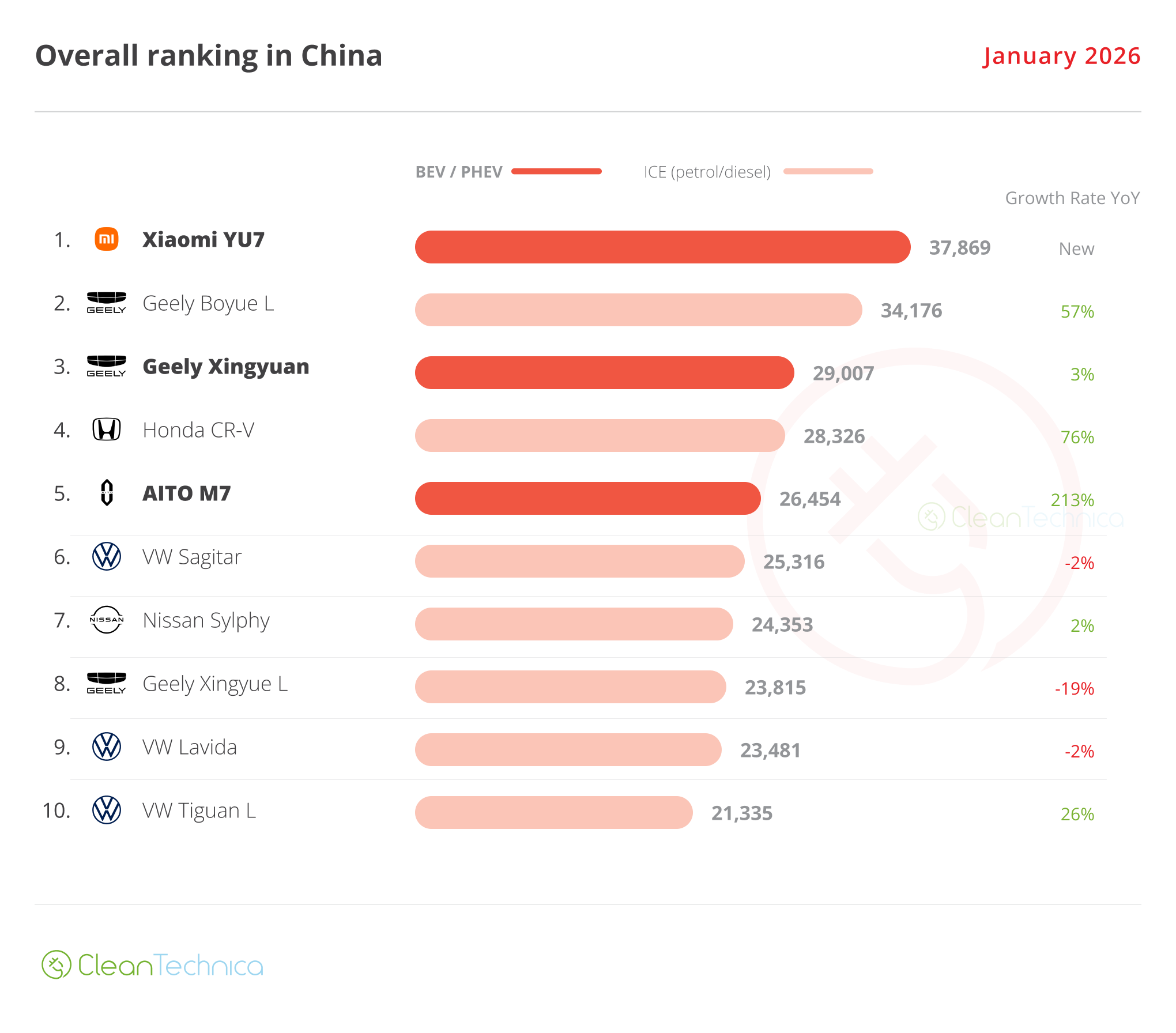

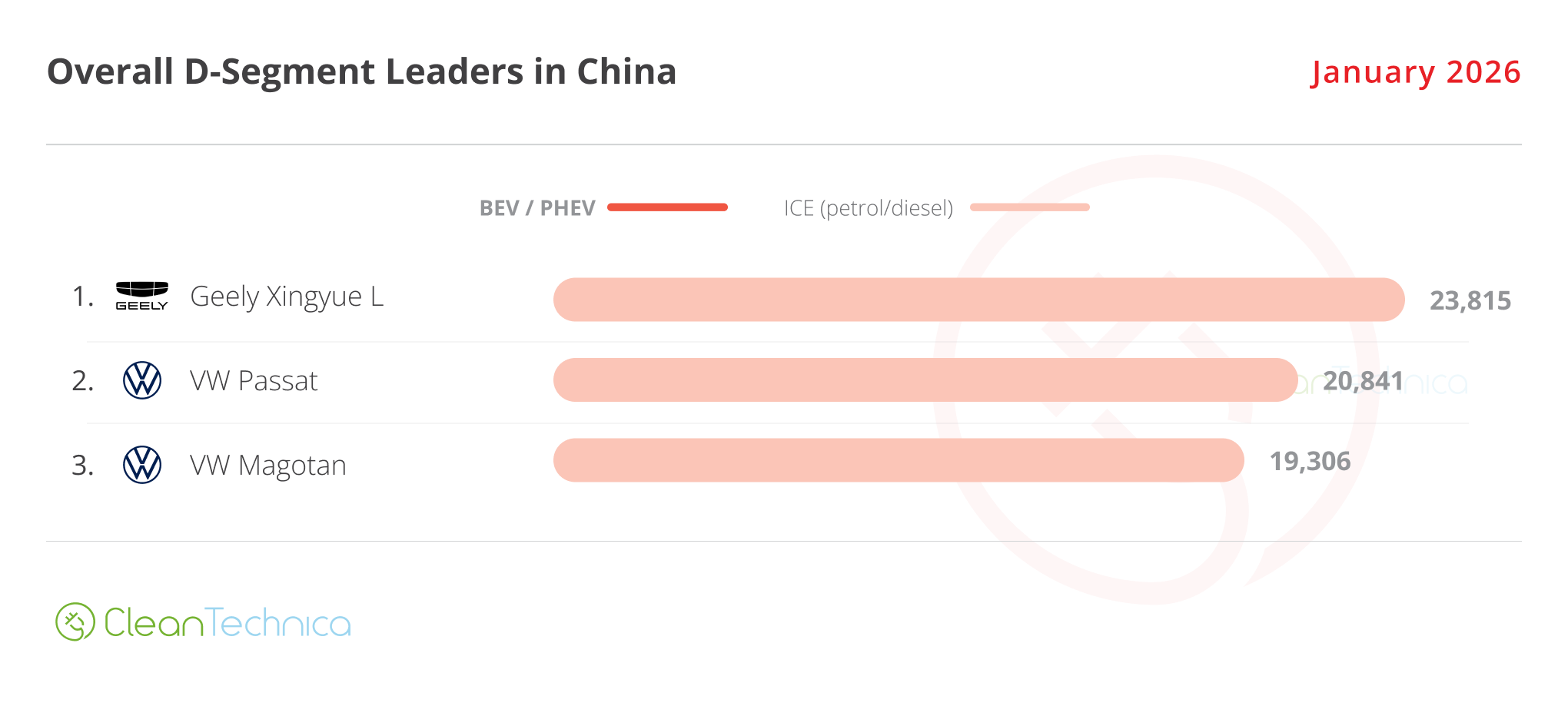

In the overall ranking, as expected, the beginning of the year has ICE models populating the top 10 — seven models in the top 10, in fact. This year, there is a sense that the market is shifting. For starters, we have a brand new model on top, with the Xiaomi YU7 sporty crossover winning the overall trophy for the first time ever. Behind it, there was a small revolution underway. The remaining podium positions went to two Geelys (Geelies?), with the Geely Boyue L ICE winning silver and the Geely Xingyuan hatchback winning bronze.

Funny enough, the most represented brands in the top 10 were Geely and … Volkswagen(!), with the German make placing three ICE models, giving a certain retro feel to the overall top 10. The AITO M7 was the third plugin model, in 5th.

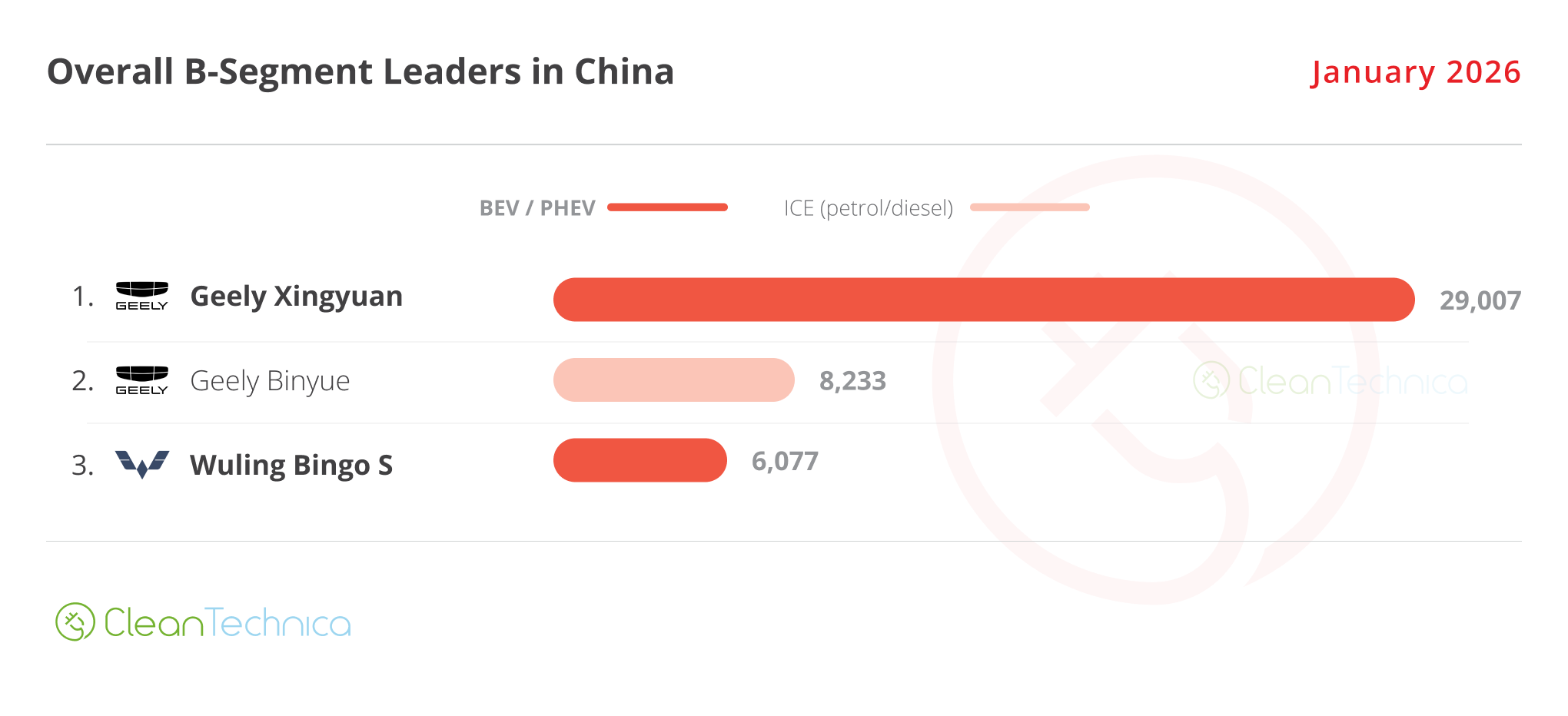

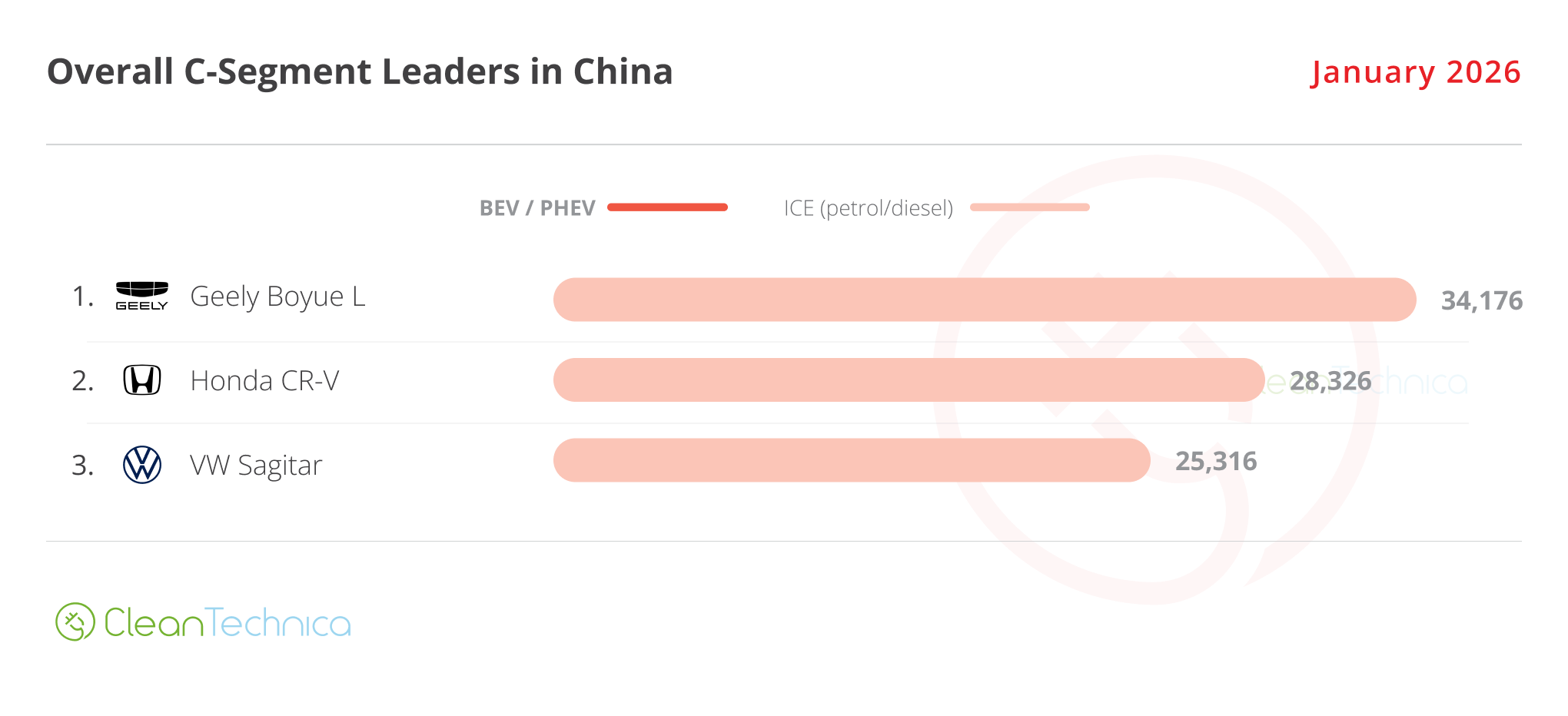

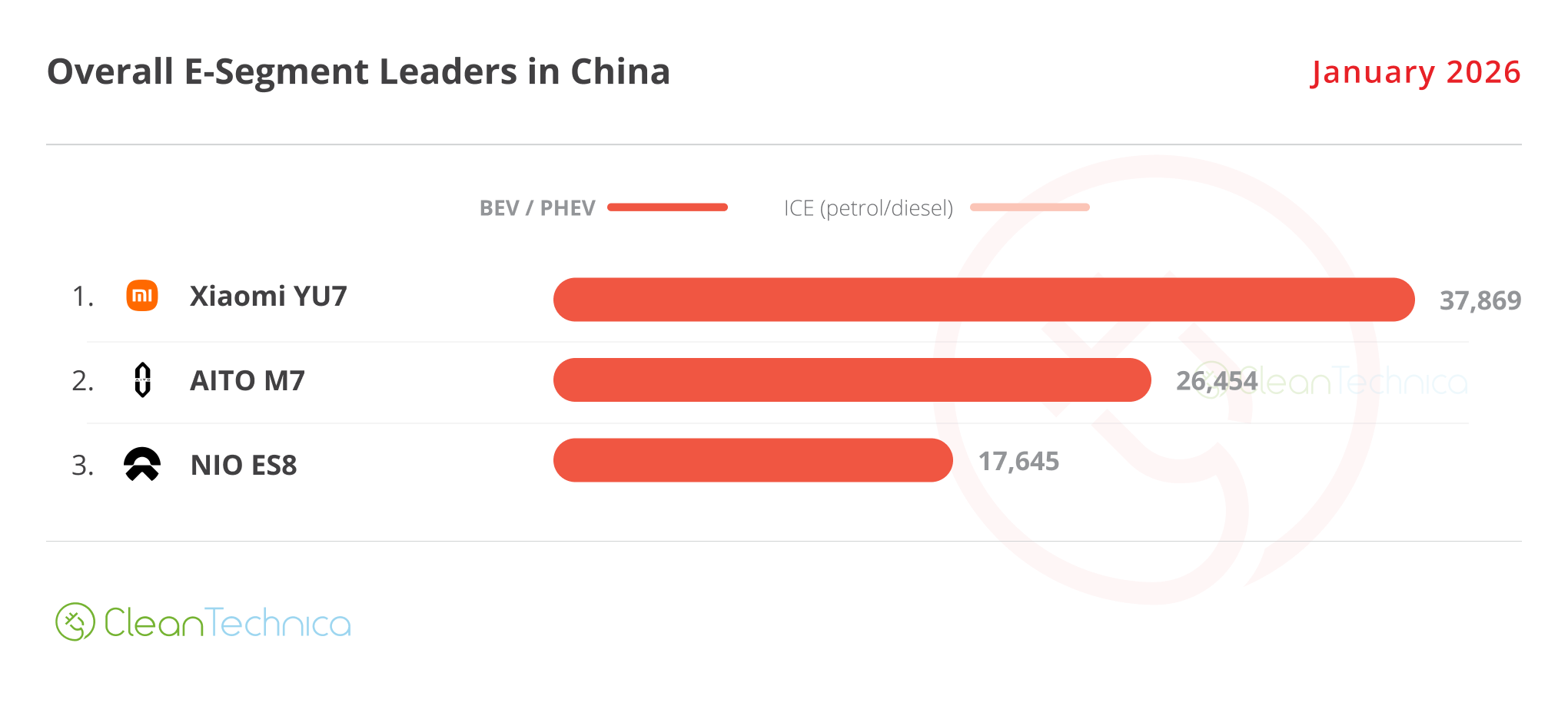

Looking at the best sellers in several size categories, all but the C (compact) and D (midsize) segments have plugins leading each category. In fact, in these two categories, all top three positions were filled by ICE models.

The biggest surprises were the Geely victories in the C and D segments — from the ICE models Boyue L and Xingyue L, respectively.

They have beaten the missing in action BYD competition and Tesla Model Y, which haven’t even joined the podium in those size categories! It was a great month for Geely, which placed five representatives on the category podiums, all while BYD had … zero. Nada.

This is a whole letter of intention from Geely. With Geely’s sprawling lineup, albeit still partly relying on ICE (internal combustion engines), the fact is that if BYD thought it had the Chinese market locked in for the next few years, it might have been wrong and Geely could be the one to spoil BYD’s plans…. Maybe already this year.

Focusing only on plugins, and illustrating the changing trends of the Chinese EV market, only the Geely Xingyuan has repeated its top 5 presence 12 months later. And all top 5 positions went to five different OEMs. Now that’s what I call (welcome) diversity!

Here’s a closer look at January’s top 5 best selling models:

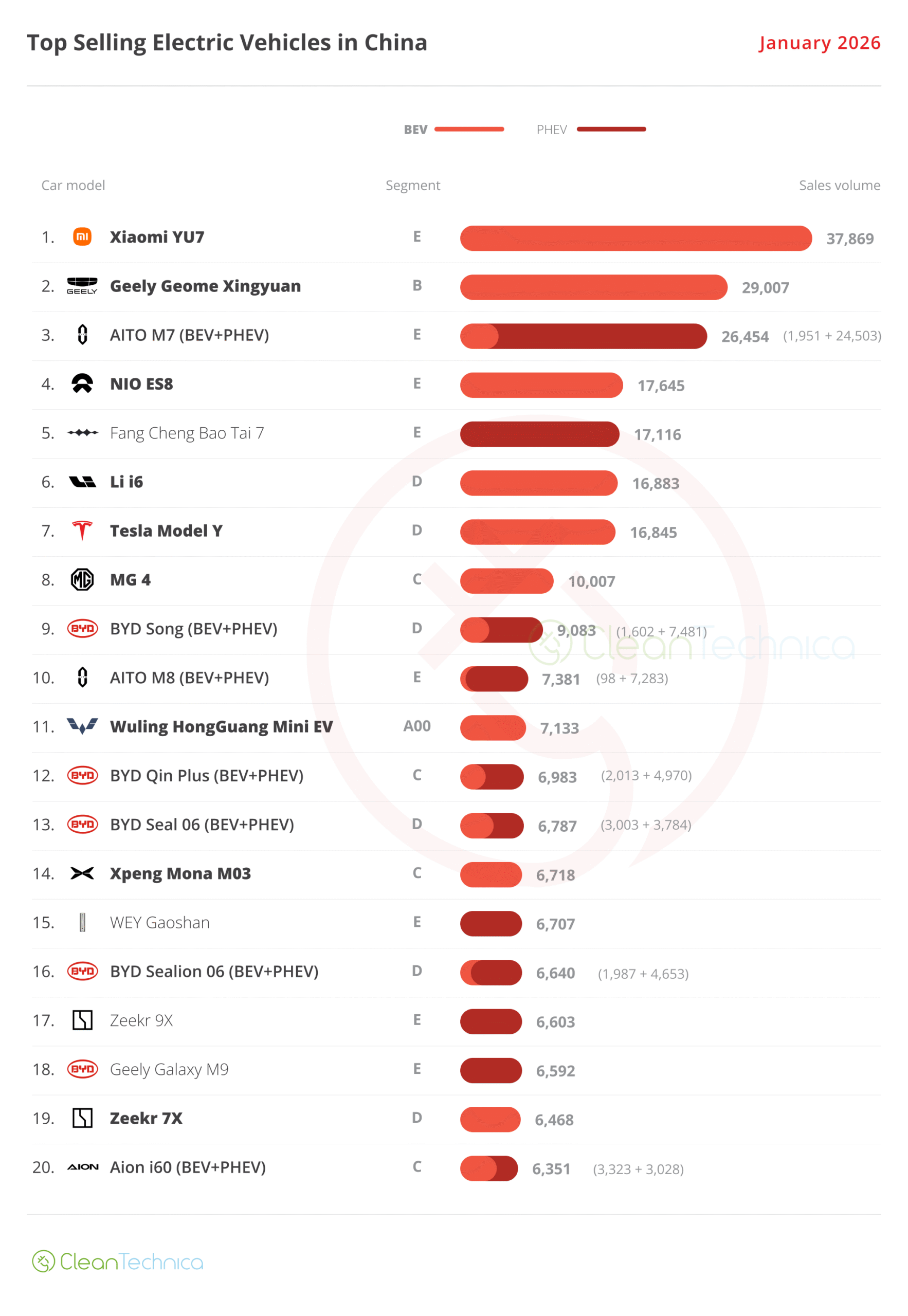

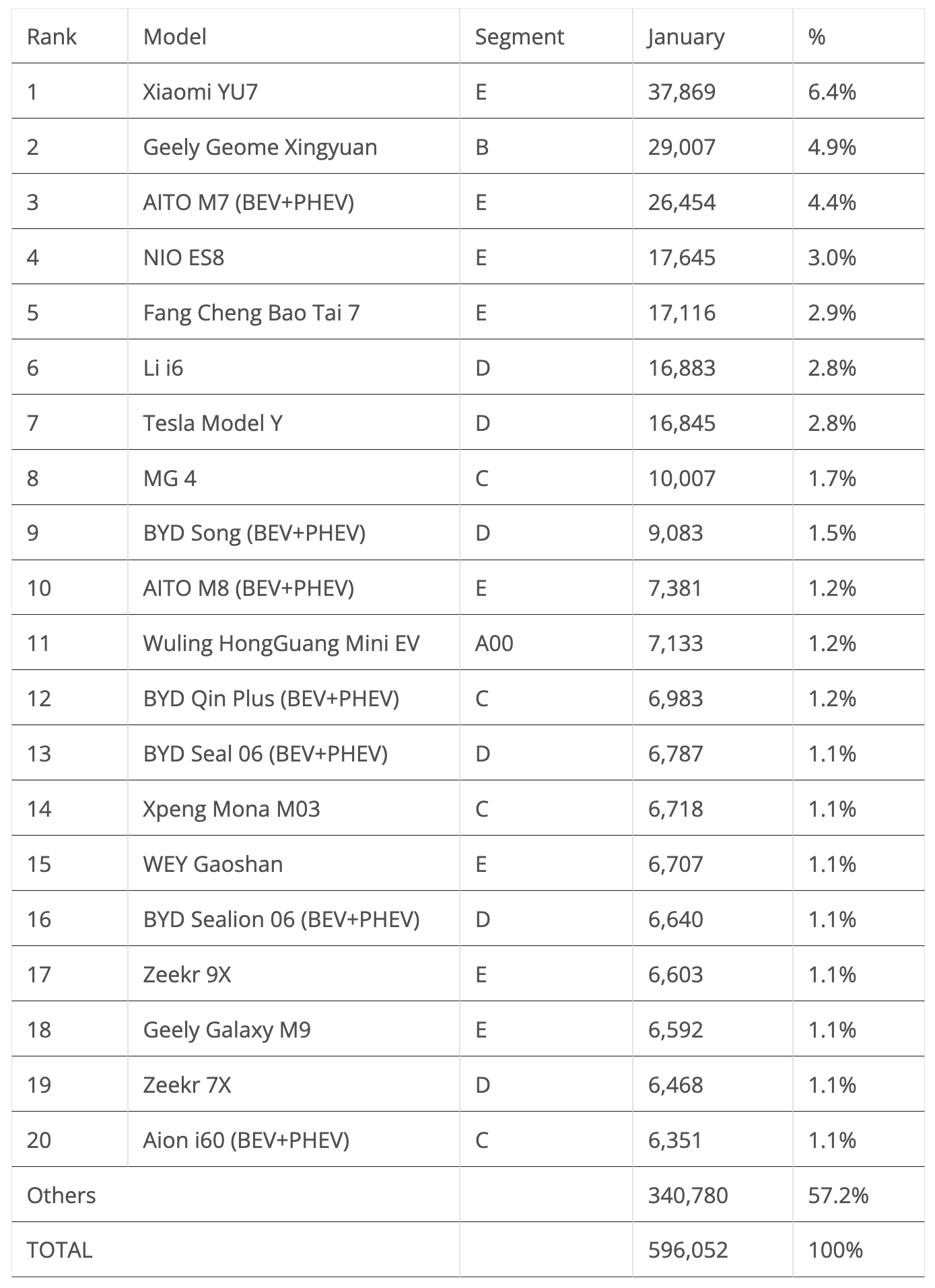

#1 — Xiaomi YU7

2025’s Car of the Year, Xiaomi’s YU7 continues to impress, registering a near-record 37,869 deliveries in January and collecting its first monthly best seller award. The YU7 got hundreds of thousands of locked-in orders within hours. So, a partial loss of incentives couldn’t slow things down for the sporty crossover, as Xiaomi still has a sizable waiting list for its new star player. The YU7 will surely be a model that will collect plenty of podium presences (and wins?) in the coming months.

#2 — Geely Geome Xingyuan

A BYD Dolphin for BYD Seagull money — at least, that’s how Geely’s internal memo might have described the Geome Xingyuan when developing its latest hatchback. And with an interesting name, as Xingyuan translates as “wishing upon a star,” is Geely wishing on a star to take BYD’s leadership position? Well, that’s what the Xingyuan did in the B-class category. It obliterated BYD’s models as well as the rest of the competition, without any margin of doubt. What does this hatchback have that makes it so special? Besides all the support that comes from a leading OEM like Geely, it has a rounded, sensible design, somewhere between a Wuling Bingo and a Smart #3. Starting with an 80,000 CNY (+/-$11,000) price, the buyer gets a 30 kWh LFP battery from CATL, which is nothing to write home about until you realise that its price places it closer to the BYD Seagull (70,000 CNY for the 30 kWh version) than the BYD Dolphin (100,000 CNY). In January, the Geely model hit 29,007 registrations.

#3 — AITO M7

The second generation AITO M7 is another example of the progress that Chinese EVs are making. After starting out its career in 2022, with an okay(ish) design and already respectable specs (EREV powertrain, 40 kWh battery), despite being based on an ICE platform, only three years later, in 2025, a brand new generation has launched — with a sleeker design, completely new platform, improved specs (53 kWh battery for the EREV version, 100 kWh for the new BEV version), all for around $35,000. Which is not a bad price for a full size, three row SUV….

#4 — NIO ES8

Thanks to the new generation, the 3rd ever since it was launched in 2018, NIO’s big SUV scored 17,645 registrations in January, providing the startup company its first top 5 finish and much needed volume in its quest to reach profitability. Not exactly cheap — it starts at around $57,000 — the truth is that NIO has thrown everything it has into the new ES8. The company is looking to redefine luxury with its new, huge SUV, now at 5.3 meters. Will this level of sales be sustainable in the future? A year ago, I would say it was unlikely, but with big SUVs being the latest fashion trend in China, and BEVs outrunning PHEVs recently, it could be the case that the ES8 might be the right model at the right time.

#5 — Fang Cheng Bao Tai 7

BYD’s premium arm Fang Cheng Bao has a success on its hands. This big Land Rover SUV, the Tai (Ti?) 7, scored 17,116 registrations last month. This Chinese Defender has an EREV powertrain with either 27 or 36 kWh batteries, allowing around 100 km (60 miles) of range — which might not sound much compared to the 52 kWh battery of the Lynk & Co 900, another Land Rover-inspired EREV SUV, 0r the 70 kWh of the Zeekr 9X, the Rolls Royce–inspired flagship EREV SUV from the Geely stable, but then again, the Tai 7 ($25,000) is almost half the price of the Lynk & Co model and almost one third of the price of the Zeekr…. Thanks to a successful boxy design, competitive specs, and a nice interior, for its price range, this is one of those models that just begs to be sent overseas — going after not only the posh SUVs of premium brands, but also the gas guzzling Land Cruisers and Patrols of this world.

Below the top five, the highlight is the new i6 from Li Auto, ending the month in 6th thanks to a record 29,368 sales. While it could be considered on paper a competitor to the previously mentioned FCB Tai 7, this is a more family-orientated crossover, focused on comfort, luxury, and technology instead of off-road abilities. It should be top 5 material for 2026.

Outside the top 5, we have a few surprises, starting with the Geely Galaxy Starship 7 showing up in 6th with a record 16,883 registrations. Expect the sleek midsize SUV to become the new star player for the brand, and it’s probably hoping to win a couple of top 5 presences soon with this one.

Proving that full size models were the least affected by the incentive drop, this January we have eight representatives from this category in the top 20. Besides the aforementioned models, we should also highlight the #10 position of the AITO M8. So, the startup make placed two models on the table, all while Great Wall’s premium brand WEY placed its large MPV, the Gaoshan, at #15, and Geely Group placed two of its three behemoth SUVs in the top 20, with the Rolls-Royce-like Zeekr 9X ending the month at #17 while the more humble Geely Galaxy M9 was #18, with 6,592 registrations.

Still in the Geely stable, Zeekr placed a second model on the table. The 7X midsize SUV showing up at #19, a deserved prize for a model with such a rounded package.

Closing the table, we have an Aion model. The new i60 crossover gave much needed volume to a make that has seen better days. Will the i60 change Aion’s fortunes?

Finally, outside the top 20, the highlights come from Wuling. The crossover version of the Wuling Bingo, the Bingo S, ended fewer than 300 units behind the #20 Aion i60, while another Wuling model is ramping up and looking to join the table soon. The Starlight 560 is true to Wuling’s ethos — value for money — as this is a 7-seat compact crossover being sold for $14,000 in its BEV version. It offers a choice of a 60 or 69 kWh LFP battery. Expect this model to be popular, not only in China, but also in a number of export markets.

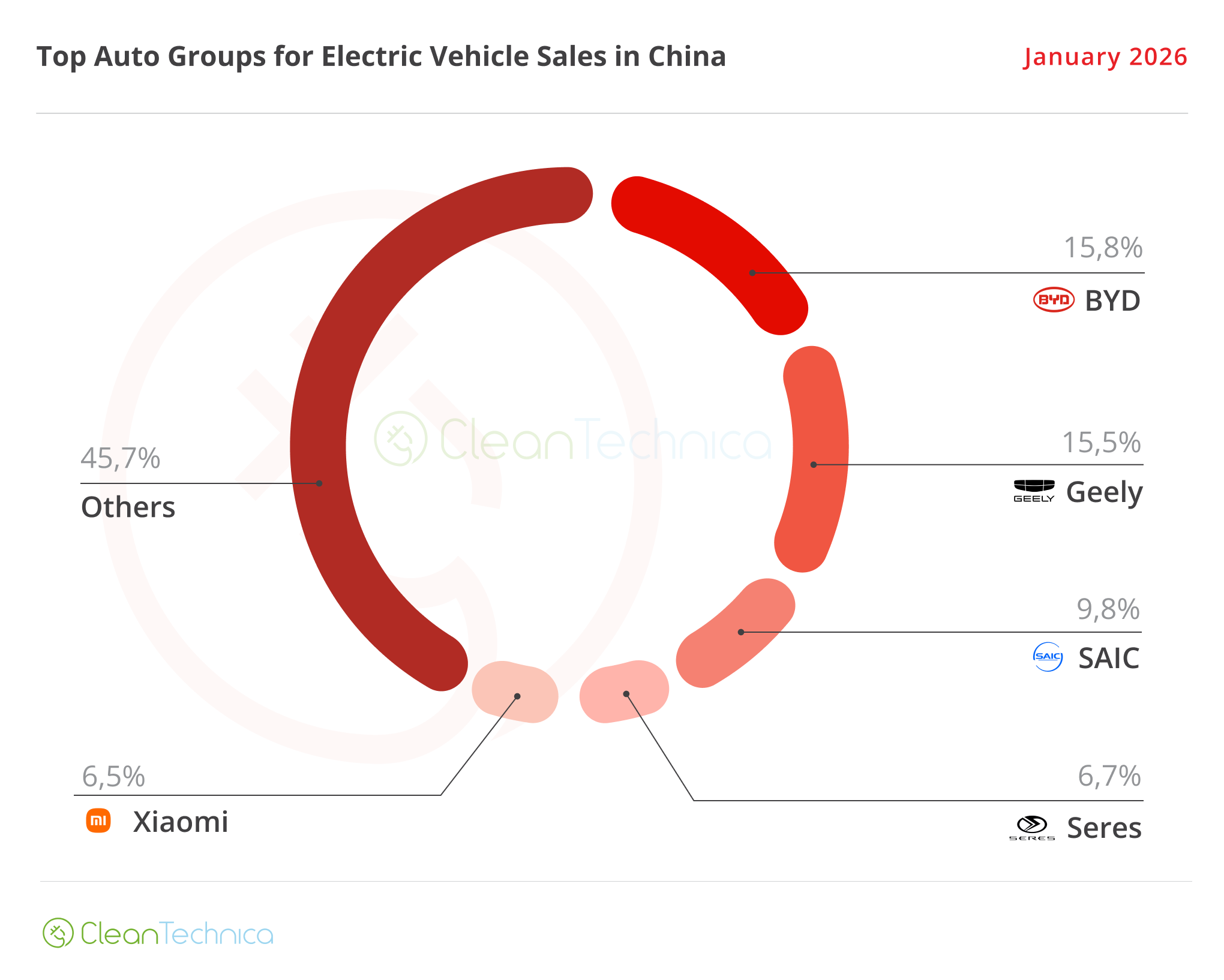

Looking at the overall manufacturer ranking, we have shock and awe — Geely (165,000 units) has beaten the competition and won the January trophy, while BYD (69,000) was only 4th!

Still more surprising, #9 Nissan was up 14% YoY in a month when everyone else saw falling sales (except … Toyota?!? which was up 4%). One wonders if this was just a blip, or if the Japanese make has again found a foothold in China.

Outside this top 10, a few mentions are due for the startups, which continue to grow fast. #12 AITO was up 83% YoY, with 40,000 registrations, while #13 Xiaomi was up 70% YoY, with 30,000 registrations. The highlight, though, was NIO. Thanks to the new ES8, it saw its sales surge 162% YoY, allowing it to be #22 in January, even ahead of #26 Tesla (-45% YoY, with 18,500 registrations).

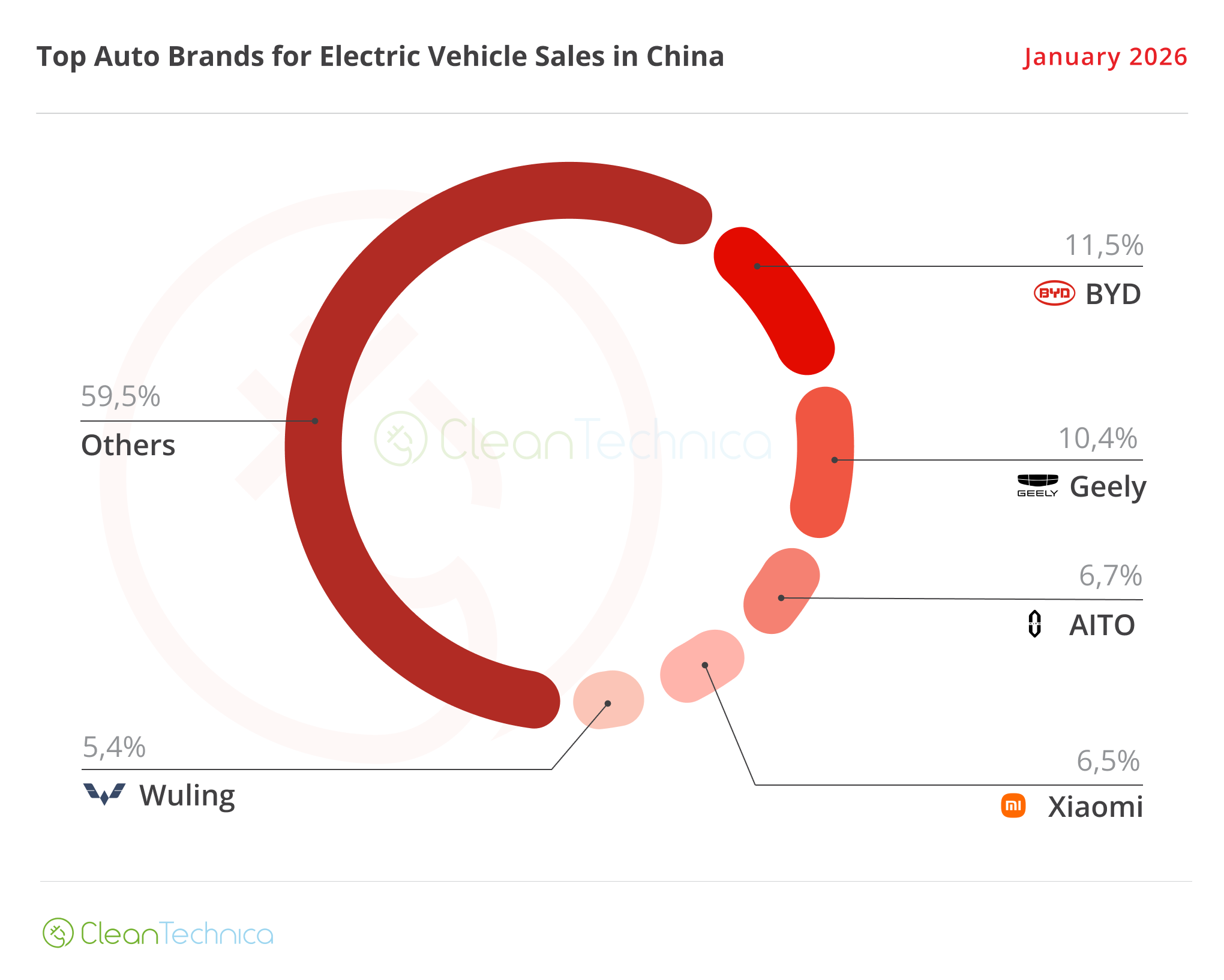

In the EV manufacturer ranking, despite losing half of its share, BYD started the year like it ended the last one, leading the table, with 11.5% share.

BUT … not only has it seen its market share split in half; it also saw Geely start the year with 10.4% share. So, the top two are separated by just about 1%!

And, while it might still be too soon to say that Geely will surpass BYD, we could see a race for supremacy in China between these two.

#3 AITO (6.7%) and #4 Xiaomi (6.5%) seemingly came out of nowhere into the top 5, while last year’s bronze medalist started this year two positions below, in 5th, with 5.4% share. True, it’s not the best start of the year for SAIC’s volume brand, but it could have been worse — after all, 2025’s 4th placed Tesla (slowly fading into irrelevance) and 5th placed Leapmotor are well below the top 5….

Just outside the top 5, we have #6 Xpeng (4.6%), which is hoping to join the table soon.

Looking at the OEM level, Geely is even closer to BYD, with only 0.3% separating the two OEMs. And with Geely firing on all cylinders, expect the Taizhou-based OEM to displace BYD sometime in the future….

SAIC is 3rd, with 9.8% share, profiting from the good results of the MG 4 and Shangjie brand. Added to the volume of the Wuling brand, Shangjie allowed the Shanghai OEM to start the year in 3rd, one position above of what it had a year ago.

Newcomers to the OEM top 5 are #4 Seres, owner of the AITO brand, and #5 Xiaomi, with 6.7% and 6.5% share, respectively.

This is more proof that it’s not only foreign OEMs feeling the heat. Tier two Chinese legacy OEMs, like Chery and Changan, are also feeling the pinch in their home market and need good export markets more than ever in order to balance out softening demand at home.

So, BYD and Geely fighting for #1 and startups eating legacy OEMs’ lunch seem to be two top items on the menu for 2026. Please bring on the popcorn, because this year should be fun to watch!…

Sign up for CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy