Economic activity in the logistics industry expanded in February, rising slightly from January and reaching its highest growth rate since June 2022, according to the latest Logistics Managers’ Index (LMI) report, released today.

The February LMI was 62.8, up from January’s reading of 62. An LMI above 50 indicates expansion in the sector; a reading below 50 indicates contraction. A reading in the 60 range indicates strong demand for logistics services.

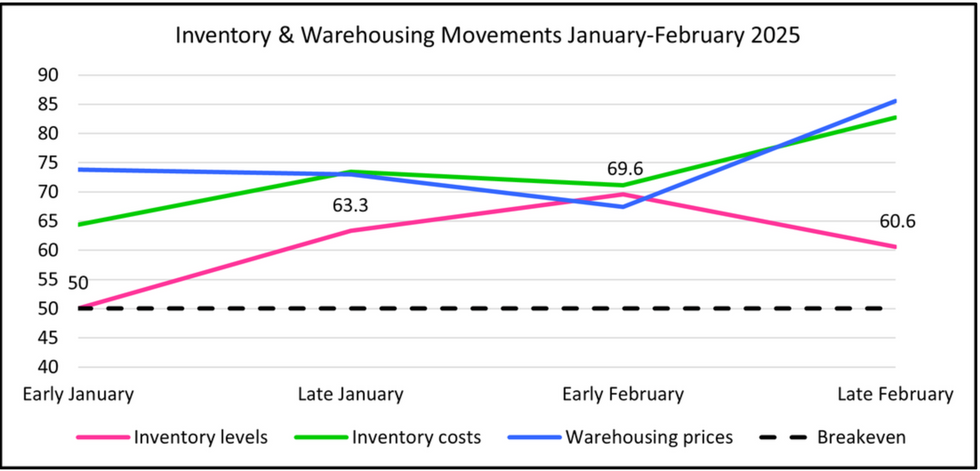

Trade policy played a large role in the monthly findings, which were driven by rising inventory levels. Inventory poured into warehouses in January and February as companies replenished from the holiday peak and attempted to avoid costs associated with tariffs on imports from China, Mexico, and Canada.

The Trump administration implemented 10% tariffs on some Chinese goods in February and then doubled them this week alongside 25% tariffs on goods from Canada and Mexico. The trade war continued on Tuesday, as all three countries announced reciprocal tariffs on U.S. goods.

Although boosting activity across warehousing and logistics, the trade situation is also contributing to higher costs, according to LMI researchers.

The LMI’s inventory levels index rose more than six points in February to a reading of 64.8. This came on top of increases in January. Combined, inventory levels for the first two months of 2025 are up nearly 15 points compared to December 2024. Inventory levels are 6.3 points higher than a year ago, and 2.4 points higher than two years ago at this time.

The spike in inventories has led to higher carrying costs and warehouse prices, as supply chains struggle to shoulder both the volume and velocity of goods coming in so far this year. Both the LMI’s inventory costs index and the warehousing prices index are growing at their fastest rates in several years, reaching 77 and above for the month, which indicates very strong growth. Those metrics reached well above the 80 mark in late February, just ahead of the March 4 tariffs, according to the researchers.

Logistics Managers’ Index

At the same time, warehousing capacity dipped during February to 50.5—hovering close to contraction, which would indicate a tightening of available warehouse space.

Together, these trends could reignite inflation, according to the report.

“These rapid rates of expansion likely [indicate] that firms are holding these high levels of inventory static and will slowly sell through them over time, which will put considerable pressure on available capacity …,” LMI researcher Zac Rogers, of Colorado State University, wrote in the February report. “This represents a move away from the [just-in-time]-centric approach that characterized 2024, and a move back towards the just-in-case … policies of 2021. This is the first time that either of these metrics has read in above 80.0 since the summer of 2022 at the height of inflation. JIC inventory practices and the associated supply costs were a major contributor to the inflation of 2021 and 2022.”

The LMI researchers noted that the U.S. economy remains strong, however, “especially relative to the world’s other leading economies.”

The LMI is a monthly survey of logistics managers from across the country. It tracks industry growth overall and across eight areas: inventory levels and costs; warehousing capacity, utilization, and prices; and transportation capacity, utilization, and prices. The report is released monthly by researchers from Arizona State University, Colorado State University, Rochester Institute of Technology, Rutgers University, and the University of Nevada, Reno, in conjunction with the Council of Supply Chain Management Professionals (CSCMP).