The maritime industry has become accustomed to riding an economic roller coaster from one year to the next. It has persevered through a host of challenges: Geopolitical conflicts that upended traditional ship routings. Hostile forces attacking ships. Government policies diverting trade flows from some nations and favoring others. Excess capacity with rock-bottom rates one year, only to be succeeded by a year of tight capacity, high rates, containers getting “rolled,” and port congestion.

It’s enough to make one wonder if there ever will be a return to normal—whatever that may be.

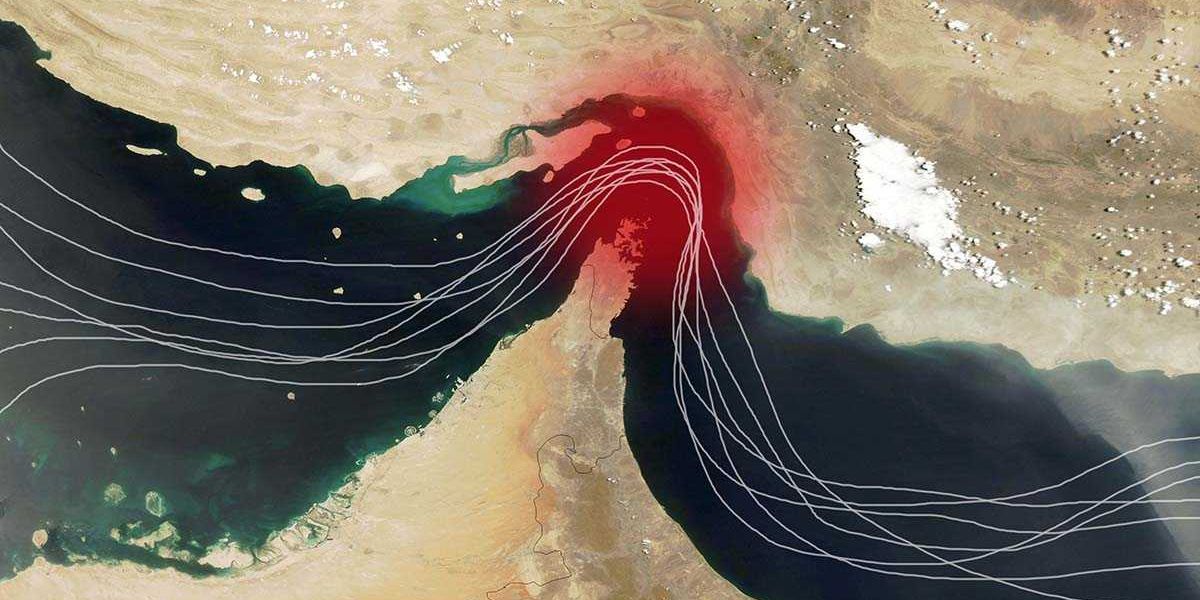

The Iran war and the resulting instability across the Middle East has had a huge impact on shipping operations to and from the region. And even as on-again/off-again discussions to end the conflict continue, a return to free flows of shipping through the Strait of Hormuz seems far off.

“We are definitely impacted and have seen our services affected to and from the region. There certainly have been a lot of changes to our ocean network,” says Michael Britton, head of North American ocean products for containership operator Maersk. “We have redeployed ships and deployed other assets, coming up with other options to continue to serve the market for general and refrigerated cargo,” he says, adding that Maersk is utilizing far more overland solutions than in the past—which are more expensive.

Through all of it, Britton emphasizes that Maersk’s top priority has been safety—of its crews, customer cargos, and vessels. “We have very much erred on the side of caution.”

At the end of the 2026 first quarter, Maersk deployed 735 container vessels, representing approximately 4.6 million TEUs (twenty-foot equivalent units) of capacity. Six dual-fuel vessels are scheduled for delivery in 2026.

SHIFTED ROUTINGS, RISING COSTS, MORE DELAYS

With this major transitway essentially closed, shippers are seeing their global over-water transit times extended—adding more complexity to supply chains. Container line operators have shifted to using various other, longer routings and port locations outside of the Strait.

“[The closure] has added from one week to a month for shipments moving between Europe, Asia, and the U.S. [which now have to go around Africa],” says Philip Damas, founder and head of Drewry Supply Chain Advisors. “Shippers are using UAE ports outside the Strait. They’re then trucking containers overland to Dubai and the upper Gulf,” he explains. The other route, he notes, is through the Red Sea and then trucking containers eastbound to the upper Gulf countries, at great expense.

“It has been very disrupting and very difficult logistically, also involving much longer transit times and increased costs, in some cases more than double,” he says.

“No one wants to send ships into the Gulf,” adds Lars Jensen, chief executive officer at ocean shipping consultancy Vespucci Maritime. “I don’t see a normalization of the container services until there is a more permanent [peace] agreement. We need more stability.”

He cites two additional factors impacting the industry as well. One is the price of “bunker” fuel and how increases are applied in carrier surcharge programs. Yet the most significant issue, Jensen believes, is when and if vessels will see safe passage through the Red Sea.

“If the prolonged Red Sea crisis is resolved, liners will go back to routing ships through the Suez Canal,” he says. Currently, the Hormuz Strait crisis has pushed ship lines to route through the Red Sea, “where they risk attack by the Houthis. Nobody wants to see ships shot at and put at risk,” he emphasizes. Once this trade lane can again be safely used, “that shortens the supply chain by two weeks as they no longer have to go around Africa.”

CAPACITY OVERLOAD ON THE HORIZON?

Overall, the ocean container market worldwide does appear to have ample capacity to support demand through the remainder of 2026 and into early 2027. At the start of summer, the industry deployed some 33 million TEUs of capacity, Drewy’s Damas reports.

As for the “order book” of new ships, “there are 1,600 ships on order, which is enormous. That’s 38% of current capacity on order, the highest we have seen in 10 years,” he notes.

And while he also expects liner operators to scrap older ships, current projections indicate “that will not be enough to balance out the excess of new ships.” He notes that the current projection for new capacity in 2027 is 3 million TEUs. Yet only 400,000 TEUs of older ship capacity is expected to be scrapped in the same time frame. “That doesn’t even make a dent,” he adds. That could foreshadow an overabundance of capacity as new ships come online and are fully deployed next year.

Damas adds that all these multiple factors are having an expected influence on container pricing. In early July, the Drewry World Container Index, the pricing benchmark widely referenced by procurement teams, showed a 9% surge to $4,530 per 40-foot TEU, reflecting rate increases on the trans-Pacific and Asia–Europe trades.

Spot rates specifically on the trans-Pacific trade route continued to strengthen, with Shanghai to New York rising 11% to $7,902 per 40-foot container, and Shanghai to Los Angeles increasing 10% to $6,349 per 40-foot container.

WHERE’S THE PEAK?

What has been the typical mid-summer to early fall peak season for ocean container demand isn’t happening this year, adds Drewy’s Damas. “We are not seeing the traditional peak season, which is from July through September,” he says.

He notes this year’s peak started in May and has largely been characterized by a series of volume spikes for a variety of reasons. Those include BCOs (beneficial cargo owners) moving freight early to avoid the next round of U.S. tariffs, a push forward of orders to restock dwindling inventories, a building up of safety stocks to prevent stockouts, and a focus on resilience instead of just-in-time inventory practices.

Vespucci Maritime’s Jensen also cites lagging inventory-to-sales-ratio data, “which has dropped sharply the last two months, matching a low in 2014” as another factor in the early May surge in container volumes. If that trend continues, he says, “then peak season demand and volumes [fueling higher] rates likely will be short-lived.”

Maersk’s Britton shares that while his company, like many, has experienced peak-season volumes, “it really has been the same type of seasonality we have seen in the past.” Maersk asked customers if they are pulling forward inventory or have changed their strategy, for whatever business reason, to address the unsettled environment. “What we have found is everyone has a different story; there is not one through line that is common to everyone,” he notes, adding “for many, it’s just normal seasonality.”

PORTS SHOWING RESILIENCE

Conflict in the Middle East has been one of several compounding headwinds that U.S. ports have had to navigate over the past year. And while the Port of New York & New Jersey “is not directly dependent on the Hormuz routing … the ripple effects on global shipping capacity, fuel costs, and carrier routing decisions have been significant,” notes Bethann Rooney, port director for the Port Authority of New York & New Jersey.

As ship lines adopted alternate routings around the Cape of Good Hope, that added weeks to transit times and increased costs across the board for shippers. Yet the NY/NJ port complex still finished 2025 as the nation’s second-busiest seaport for loaded TEUs, moving 8.9 million TEUs overall, which Rooney pointed out was a strong performance in a volatile environment.

As for peak season, Rooney echoes the trending comments of other executives. “We’ve seen indicators of an earlier, front-loaded peak season this year, with elevated volumes concentrated in June and July rather than the traditional late-summer surge,” she says. That reflects importer response to tariff uncertainty and a desire to get products on shore ahead of any post-July increases.

On the capacity side, Rooney says the NY/NJ port is closely watching forward booking data from China and Southeast Asia, vessel utilization rates on the Asia–U.S. East Coast service, and blank [canceled] sailing activity.

The Port of Oakland also has not been directly affected by the instability in the Middle East. Some container lines have added vessel calls to Oakland recently, “giving shippers more service options and greater flexibility,” notes Carolyn Almquist, the port’s business development and international marketing manager. Nevertheless, she notes, many customers have seen impacts to their supply chain from stranded or delayed cargo, higher transport costs, increased war risk premiums, and more complex challenges getting goods to market.

“More than anything, customers are looking for predictability,” she says. “Whether they are ocean carriers, beneficial cargo owners, importers, or exporters, they want reliable service and flexibility.” She notes as well that with today’s market conditions, “many customers want to make [shipping] decisions closer to the time cargo moves.”

Dr. Noel Hacegaba, CEO of California’s Port of Long Beach, issued a similar statement emphasizing the importance of stability. “The supply chain thrives on stability and predictability,” he said. “When a critical chokepoint like the Strait of Hormuz is disrupted, the effects ripple across the entire system.”

He added that while the Port of Long Beach primarily handles trans-Pacific trade with Asia, “global supply chains are deeply interconnected, and stability in global trade routes and fuel prices are major factors [that] will strengthen confidence across the whole network.” Nevertheless, given that Long Beach and Los Angeles are the entry point for some 40% of U.S. imports, Hacegaba emphasized that throughout this period, the port has remained resilient, with its terminals open and cargo moving normally.

Likewise, the Port of Los Angeles continues to move forward, processing 1,002,734 TEUs in June, making it the busiest June in the port’s 118-year history, according to Gene Seroka, the port’s CEO. Key indicators have been promising, with ships at port less than four days, truck turn times improving, and containers moving promptly off the dock, he notes.

“Thanks to our waterfront workers, this port’s humming,” Seroka adds. “Cargo demand is resilient despite everything happening in the world right now.” He’s confident the port will continue to see strong volumes. “Consumers are spending, businesses are ordering goods, and manufacturing continues to bring in parts and components, all despite the uncertainty we are seeing across the global economy.”

Closer to home, Seroka also commented on new federal regulations impacting licensing of non-domiciled drivers in the U.S. as well as the English language proficiency ruling. He notes that over the past 18 months, those rulings have impacted some 17,000 drivers and their families “in a state [California] that has 680,000 commercial driver’s licenses issued.” At the ports of Los Angeles and Long Beach, Seroka says, there were “17,000 drivers that are registered to do business at the twin ports,” more than half of which call at least once a week.

So from a truck drayage perspective, Seroka believes the ports still have ample capacity but likely will see “a little bit of fluidity, but nothing that is putting any effective downward pressure on the truck capacity here at the ports.”

PURCHASERS’ CONFIDENCE

The nation’s purchasing managers seem confident about trends in the manufacturing economy. That’s reflected in recent reports of U.S. manufacturing growth, which according to the S&P Global U.S. Manufacturing Purchasing Managers Index (PMI) for June, “remains solid despite the sharpest employment decline since 2020.

“The headline PMI registered 53.9 for June, down from 55.1 in May,” the report said. That marked the 11th consecutive month over 50.0, which is the point that separates expansion from contraction.

“U.S. manufacturers reported a further marked improvement in growth of output and order books in June,” said Chris Williamson, chief business economist at S&P Global Market Intelligence, in a statement. “Employment was nevertheless cut sharply as firms often sought to offset the rising cost of energy and raw materials,” he noted, adding that “supply chain delays and upward price pressures continue to be widely reported.”

The report noted as well that despite recent drops in energy prices and a more favorable outlook for shipping, overall business confidence, which softened during June, had fallen to an eight-month low, moderating how the market perceived the strength of the domestic U.S. economy.