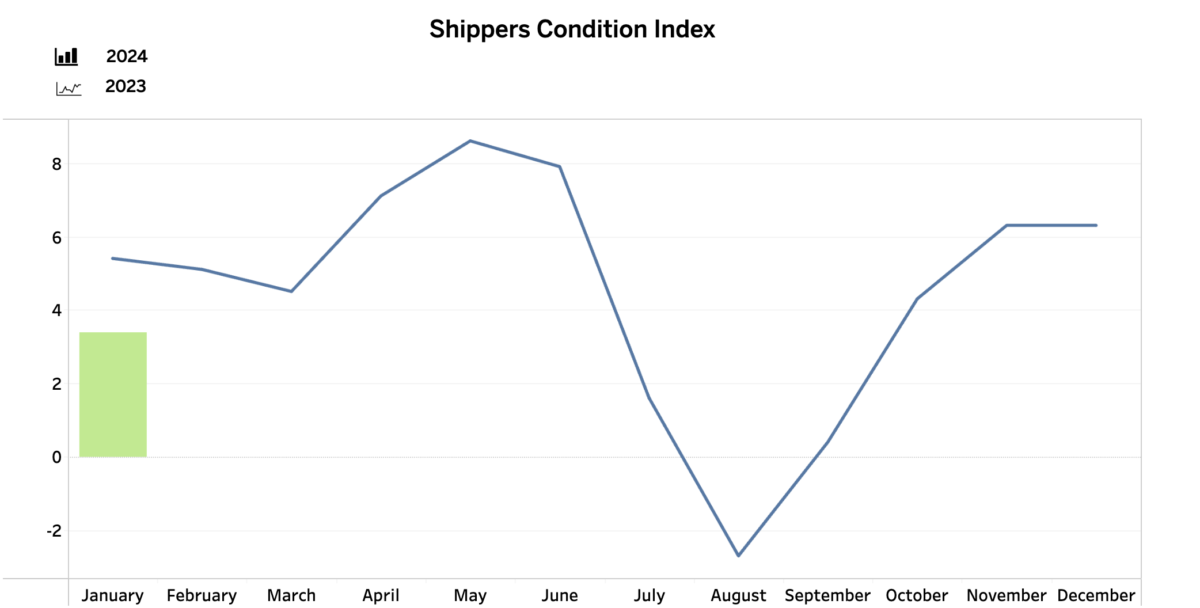

A measure of shippers’ leverage over carriers in the freight market is still barely positive after slipping in January to its lowest level since September, according to data from freight transportation forecasting and analysis firm FTR.

FTR’s January Shippers Conditions Index (SCI) fell 3 points in January to a reading of 3.4. While still positive, the SCI was the weakest it had been since September, Bloomington, Indiana-based FTR said.

The most significant changes from December conditions were less favorable freight rates and a slowdown in fuel cost decreases. One factor related to rates was the brief spike in trucking spot rates due to winter weather in the middle of the month. FTR said it expects the SCI now to move closer to neutral market conditions, which are represented in the index by a reading of 0.

“Until recently, market conditions for shippers were reliably favorable except at times when diesel prices soared in relatively short periods,” Avery Vise, FTR’s vice president of trucking, said in a release. “Core freight market dynamics – freight rates, utilization, and volume – have been consistent positives for shippers. That situation is changing, albeit gradually. We expect more muted conditions through 2024, and shippers should anticipate modestly more challenging market conditions by early 2025.”

The index tracks the changes representing four major conditions in the U.S. full-load freight market: freight demand, freight rates, fleet capacity, and fuel price. Combined into a single index number, the score represents good, optimistic conditions when positive, and bad, pessimistic conditions when negative.

Those results echo a report this week from fellow freight industry analyst firm ACT Research, which said its own index detected “green shoots” of improvement for the long-suffering full truckload sector.

ACT said its For-Hire Trucking Index reflects the continued recovery of the freight market, pointing to a 2.3 point increase in its Volume Index for February to 52.3, seasonally adjusted, from 50.0 in January. At the same time, the firm’s Capacity Index decreased by 1.1 points m/m to 48.7 in February.

“The US economy continues to surpass expectations, and with goods prices now declining, retail sales are likely to recover in the coming months,” Carter Vieth, research analyst at ACT Research, said in a release. “Supporting the retail recovery is solid real income growth, a strong job market, and the end of the post-pandemic services boom. And after an 18-month destock, signs point to a restock beginning.”