US met coal offers limited relief for India’s steel energy security: IEEFA – Indian PSU

India imports around 90% of its metallurgical coal requirements and plans to nearly double its steelmaking capacity by 2030. Although the country has broadened its supplier base in recent years, its move to diversify metallurgical (met) coal imports toward the United States is unlikely to significantly reduce the risks associated with supply disruptions and price volatility.

As India seeks to reduce its dependence on Australian met coal, the ongoing West Asia conflict has once again underscored the vulnerabilities of continued reliance on imported fossil fuel-based raw materials, highlighting the urgent need for a stronger and more resilient energy security strategy for the steel sector.

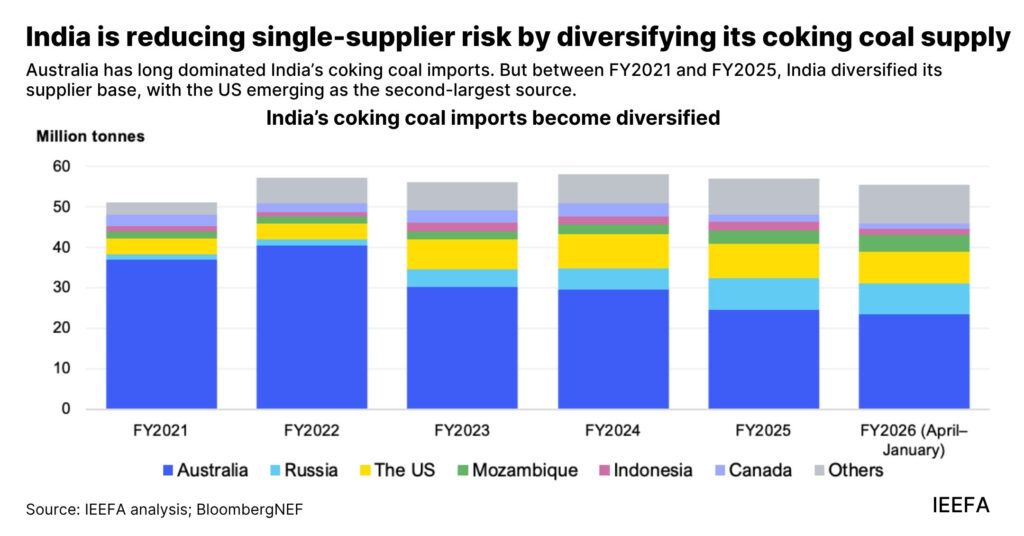

Under the recent bilateral trade agreement with the United States, India could increase imports of metallurgical coal from the US as part of its broader effort to diversify away from Australian supplies. The US has already emerged as India’s second-largest supplier, increasing its share from around 8% in FY2021 to nearly 15% in FY2025. However, according to the Institute for Energy Economics and Financial Analysis (IEEFA), the benefits of this diversification remain limited.

Australia continues to dominate global metallurgical coal exports, meaning that any disruption to Australian supply has an immediate impact on global pricing. When buyers turn to alternative sources such as the US, those markets also witness price escalation.

This was evident after severe flooding in January 2026 disrupted mining activity in Australia’s key metallurgical coal region of Queensland. The supply shock triggered a sharp rally in global met coal prices, with US coal prices also climbing as international buyers scrambled for substitute cargoes. By February 4, prices had risen by more than 50% compared with March 2025 levels.

Climate-linked weather disruptions in Australia are expected to become more frequent, suggesting that such global price shocks may occur with increasing regularity in the coming years.

At the same time, the West Asia conflict has pushed energy security concerns to the forefront of the global industrial agenda. For India, the message is clear: supplier diversification alone cannot provide long-term protection.

IEEFA argues that policymakers must move beyond merely changing the source of imported coal and instead focus on reducing India’s structural dependence on metallurgical coal itself.

Key Takeaways

- Diversifying metallurgical coal imports away from Australia toward the US offers India only limited protection against volatility in prices, freight rates and supply disruptions, as global coal pricing remains tightly linked to Australian production.

- The West Asia crisis is further exposing the freight disadvantage of US-origin coal. Longer shipping distances, rising bunker fuel costs and elevated insurance premiums are making American cargoes increasingly expensive.

- US metallurgical coal export capacity is limited and is not expected to expand sufficiently to replace Australian volumes at the scale India would require.

- Disruptions in Australia continue to trigger immediate global price spikes, which are rapidly reflected in US coal prices as well.

- To build durable energy security, India must gradually reduce dependence on coal-based blast furnace technology and accelerate the transition to scrap-based electric arc furnace (EAF) steelmaking and green hydrogen-based steel production.

A new briefing note by the Institute for Energy Economics and Financial Analysis (IEEFA), titled “US met coal offers limited relief for India’s steel energy security,” has found that India’s push to diversify metallurgical coal imports toward the United States is unlikely to significantly reduce the steel sector’s exposure to supply disruptions and price volatility.

The report notes that although the shift is being supported by recent bilateral trade engagement between India and the US, as well as heightened energy security concerns triggered by the West Asia conflict, several structural factors weaken the case for American coal as a meaningful long-term substitute. These include global price linkages, higher freight costs, limited US export capacity and technical constraints within Indian steel plants.

Australian supply continues to dictate global prices

Despite India’s efforts to broaden its supplier base in recent years, Australia still accounts for nearly half of global seaborne metallurgical coal exports. This overwhelming dominance means that any disruption in Australian production or logistics quickly triggers price spikes across the global market, including in US-origin coal.

A clear example emerged in January 2026, when heavy rainfall and flooding in Queensland—widely regarded as the world’s most critical metallurgical coal exporting region—disrupted mining operations and transportation networks.

The resulting supply shock sent benchmark premium Australian hard coking coal (HCC) prices soaring to USD 252.5 per tonne (Rs 23,404 per tonne) on February 4, marking an 18-month high and representing an increase of more than 50% over the lows recorded in March 2025.

This sharp rise highlighted the continued vulnerability of the global metallurgical coal market to weather-related disruptions in Australia and demonstrated that alternate suppliers such as the US remain tied to the same international pricing cycle.

Freight costs and declining US export capacity weaken substitution prospects

The growing role of US coal in India’s import basket has been aided by changing trade flows and recent bilateral agreements. However, the IEEFA note points out that American coal faces clear structural disadvantages.

Australian cargoes enjoy a significant logistical advantage due to much shorter shipping distances to Indian ports, resulting in lower freight costs and faster delivery timelines. In contrast, US cargoes travel much longer maritime routes, substantially increasing transportation expenses and reducing landed cost competitiveness.

“Freight economics are a key factor. The longer distance for US cargoes means higher freight costs, now exacerbated by the West Asia crisis and the impact on shipping fuel,” said Simon Nicholas, co-author of the briefing note and Global Lead Analyst – Steel at IEEFA.

The report further notes that US metallurgical coal export capacity remains limited and is expected to decline in the coming years, even as India’s import demand continues to rise. This widening mismatch significantly reduces America’s ability to serve as a dependable large-scale replacement for Australian supplies.

Another critical limitation is technological.

Indian steelmakers are increasingly adopting stamp-charging technology, a coking process specifically optimised for blends of domestic and Australian coal. This reduces the compatibility of US-origin coal in several existing steel plants and makes supplier switching both operationally difficult and financially expensive.

Diversification alone cannot solve India’s energy security challenge

IEEFA concludes that merely importing coal from a larger number of countries does not address India’s underlying steel energy security risks.

“Even with diversified supply, India will remain exposed to global price volatility, supply disruptions and climate-related risks in major exporting regions,” said Saumya Nautiyal, Energy Finance Analyst – South Asia at IEEFA and co-author of the note.

According to the analysis, the more durable solution lies not in changing import origins, but in reducing India’s long-term dependence on imported metallurgical coal itself.

To achieve this, IEEFA recommends accelerating the transition toward scrap-based Electric Arc Furnace (EAF) steelmaking and scaling up green hydrogen-based steel production.

Domestic green hydrogen, in particular, is emerging as a strategic opportunity at a time when fossil fuel markets remain vulnerable to climate shocks, freight disruptions and geopolitical tensions.

By reducing dependence on imported coking coal over the long term, India would be in a stronger position to build a more resilient, competitive and future-ready steel sector aligned with both national energy security objectives and decarbonisation commitments.

The writer of this article is Dr. Seema Javed, an environmentalist & a communications professional in the field of climate and energy