Support CleanTechnica’s work through a Substack subscription or on Stripe.

The idea of a European green steel premium has become widely accepted over the past several years. It rests on the belief that Europe can decarbonize its steel sector domestically, absorb higher production costs through a mix of policy support and buyer willingness, and maintain industrial competitiveness while doing so. This belief is reinforced by Europe’s long steelmaking history, its climate policy ambition, the introduction of the Carbon Border Adjustment Mechanism, and early offtake announcements from automotive and industrial buyers. The narrative is appealing because it suggests continuity. Europe keeps making steel, just cleaner, and the market rewards that effort with a premium.

The problem is not that the goal is wrong. The problem is that the conditions required for a durable premium are not lining up. For a premium to persist, buyers must be able to pay it without losing competitiveness, producers must be able to deliver at scale without relying on permanent subsidies, and costs must show a credible path toward convergence. In Europe today, buyer tolerance is narrowing, producer economics are deteriorating, and cost convergence is moving in the wrong direction. These failures are not independent. They reinforce one another.

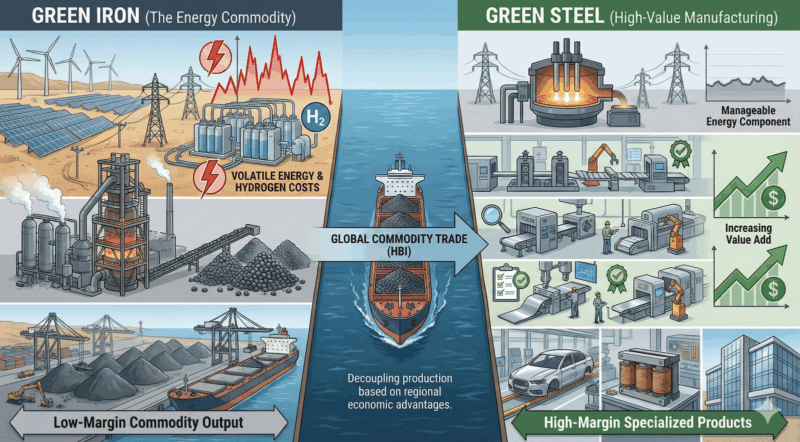

A central source of confusion is the way steel is discussed as a single product. Steelmaking combines two very different industrial stages. Ironmaking is a bulk, energy intensive, commodity process. Steelmaking and finishing are where metallurgy, precision, and product differentiation appear. When these are collapsed into the phrase green steel, strategies become muddled. The economics of iron production dominate total cost and emissions. The economics of steel finishing dominate value capture. Treating them as one problem leads to policies that try to force value where none naturally exists.

Green iron production has clear physical and economic requirements. It needs very cheap renewable electricity, typically sustained below $30 per MWh. It needs high utilization electrolyzers or other reduction systems so capital costs are spread across large output. It needs abundant land for generation, transmission, storage, and industrial facilities. It needs reliable water supply for electrolysis and processing. It needs iron ore at global scale, measured in tens or hundreds of millions of tons per year, not prospective deposits or pilot mines. It needs ports or integrated rail to move large volumes efficiently. Finally, it needs political and contractual stability so investors can finance assets with 20 to 40 year lifetimes.

When iron ore scale is treated as a hard constraint rather than an afterthought, the list of plausible green iron regions narrows sharply. Australia produces more than 900 million tons of iron ore per year and already operates mine rail port systems designed for export. Brazil produces over 400 million tons per year, with high grade ore from Carajás, deepwater ports, and an established DRI and HBI industry. These two countries alone account for the majority of globally traded iron ore and sit at the center of any realistic green iron transition.

Canada produces roughly 60 to 70 million tons of iron ore per year, concentrated in Quebec and Labrador. The ore quality is good and access to hydroelectric power is strong, but scale is limited and expansion timelines are long. Canada can support regional or captive green iron production but does not set global prices. Parts of North Africa, notably Mauritania, export around 13 to 15 million tons per year. Renewable resources and proximity to Europe are attractive, but ore scale is one to two orders of magnitude smaller than Brazil or Australia and infrastructure remains thin. These regions can play niche roles or function as processing hubs importing ore, but they are not anchors for bulk supply.

The United States produces about 45 to 50 million tons of iron ore annually, mostly from the Mesabi Range. This production is inward facing and tightly linked to domestic steelmaking. Export oriented green iron for Europe is unlikely given domestic demand and policy incentives. The Middle East has minimal domestic iron ore and would rely entirely on imported ore. It can function as an energy and processing hub but not as an ore based producer.

Europe does not appear on this list. It lacks iron ore at scale, has some of the highest industrial electricity prices in the world, faces land and permitting constraints, and is in the process of socializing large infrastructure costs across electricity consumers. These costs do not disappear when steel plants electrify. They compound. Electricity prices feed into hydrogen costs through electrolysis, then feed again into electric arc furnaces and finishing operations. The result is a structural cost disadvantage that policy cannot fully offset.

Hydrogen based ironmaking amplifies this disadvantage in Europe. Electrolytic hydrogen production is capital intensive and electricity intensive. In regions with cheap power and high utilization, hydrogen costs may approach $2 per kg over time. In Europe, recent analyses and project disclosures suggest costs closer to $4 to $6 per kg when grid charges, network costs, and utilization penalties are included. Each $1 per kg increase in hydrogen cost adds roughly $50 to $60 per ton of iron. This quickly pushes green iron hundreds of dollars per ton above global benchmarks.

This dynamic mirrors what has been seen in hydrogen infrastructure more broadly. Building expensive carrier infrastructure ahead of firm demand leads to underutilization. Underutilization drives up unit costs. Those costs are socialized through electricity tariffs. The system becomes more expensive, not more competitive. Green iron projects in Europe are caught inside this loop.

Alternatives such as electrified biomethane DRI deserve careful treatment. Biomethane can displace fossil gas in existing DRI plants, avoiding the need for large scale hydrogen. When paired with electrified heating and carbon capture, lifecycle emissions can approach or even cross into net negative territory depending on accounting assumptions. The challenge is volume. Sustainable biomethane supply in Europe is limited and competes, realistically, with dunkelfaute energy storage and chemical feedstock uses. These pathways are valuable for specific plants and products but cannot support current bulk iron decarbonization volumes. Part of the solution, yes. All of the solution, no.

Once ironmaking is separated from steelmaking, the rational industrial strategy becomes clearer. Iron should be produced where ore and cheap energy coexist. That iron should be moved as a solid intermediate, such as direct reduced iron (DRI) or hot briquetted iron (HBI). Shipping solid iron units is mature, low risk, and far cheaper than transporting hydrogen. Losses are minimal. Carbon intensity can be verified physically at the production site using process data and material flows rather than certificates and book and claim systems.

Europe’s competitive advantage lies downstream. It has deep expertise in specialty steels, automotive grades, electrical steels, and high precision rolling and finishing. These products command premiums because performance matters more than raw material cost. Steel is a small share of total product value in these applications. This is where green premiums—and jobs—survive.

Reframed this way, the green premium is not a surcharge on bulk steel. It is value capture on high performance products made with low carbon inputs. The premium follows value density, not moral intent. Trying to attach large premiums to commodity iron production in Europe is fighting physics and global trade patterns.

Demand side realities reinforce this conclusion. European automotive manufacturers are under sustained margin pressure as they transition to electric vehicles and compete with Chinese producers. Battery costs dominate vehicle economics. Steel cost increases of $100 per ton translate into roughly $80–$120 per vehicle before absorption, and still tens of dollars per vehicle after partial pass-through. This matters when margins are thin and price competition is intense. Willingness to pay survives in flagship models and specialty components but not across entire fleets.

Policy tools such as CBAM help align carbon costs between domestic and imported materials, but they do not fix geography. CBAM equalizes emissions pricing. It does not lower electricity costs or improve electrolyzer utilization. It supports imported green iron just as effectively as domestic production. Treating CBAM as a shield for high cost domestic ironmaking misreads its function.

The risk for Europe is defending the wrong part of the value chain. Pouring capital into bulk green iron production raises electricity prices, strains grids, and weakens downstream competitiveness. The same dynamic has been observed in hydrogen infrastructure planning. The assets become stranded or underutilized while costs persist.

A more resilient path is available. Europe can maximize scrap recycling, expand electric arc furnace capacity, import green iron from ore and energy advantaged regions, and focus public support on high value steelmaking and finishing. This is also where the jobs and intellectual capital advantages are. Electricity policy should prioritize affordability and reliability for downstream industry rather than subsidizing structurally high cost inputs.

The uncomfortable conclusion is that green premiums follow value, not virtue. Europe can lead in low carbon steel, but only by aligning strategy with industrial reality. Bulk green iron belongs where ore and energy are cheap. European leadership belongs in turning that iron into products the world is willing to pay more for, because they perform better, last longer, and meet demanding specifications with lower lifecycle emissions.

Sign up for CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and high level summaries, sign up for our daily newsletter, and follow us on Google News!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one on top stories of the week if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy